A senior associate at the FCA said in a confidential letter that “a number of weaknesses were identified [at Lendy] around the accuracy and quality of information” provided to retail investors some 10 months before the city regulator gave the ultimate seal of approval in the form of full authorisation.

It took almost two years after the date of this letter before the FCA finally pulled the plug on the platform. According to reports made by the joint administrators’ the members of the public who invested stand to lose up to 93% of their money.

Please donate to the Cheese Fund to support crowd-funded journalism of the P2P sector.

Reporting by Daniel Cloake.

Problems identified include:

- Investments in loans to a bankrupt borrower allowed to continue for 15 months

- Loans to a borrower “‘blacklisted’ by a number of major lenders due to historic non-performing loan portfolios“

- Lendy having a personal interest in a loan and potentially selling out prior to default

The letter

In August 2023 the mouseinthecourt exclusively reported that a confidential 2017 FCA report revealed a catalogue of concerns at the firm.

The report concluded that “once the FCA has considered the firm’s response, if our concerns have not been addressed, it is likely that we will invite the firm to [the FCA office] to discuss the application“.

We can now reveal that the FCA did visit the firms offices in early October 2017.

A 3-page-letter, exclusively seen by the mouseinthecourt, was sent by a senior associate in the retail finance & debt department at the FCA. The letter reveals the cause of the visit was to “help us better understand the way the firm operates and to discuss systems and controls”.

The senior associate confirms that “a number of weaknesses were identified around the accuracy and quality of information provided to lenders buying” loans on the platform.

This information is said to form “the foundation of which lenders will base their decision to lend or not” and “it is therefore vital that, at the time of purchase, a lender sees information that is an accurate reflection of the loan, the security and the borrower”.

Examples of this information was said to include loans in which the borrower had failed to comply with the specific terms of the loan agreement. The city regulator found that “although the firm was aware of the default event, the information was not passed on to existing lenders, who had funded the loan, or to subsequent buyers on the secondary market.”

“The weaknesses identified are a breach of several of our Handbook rules and also of our Principles for Businesses” it was concluded.

Attached as an appendix to the letter is a “summary of the weaknesses identified in the file reviews” carried out by the FCA.

These show an extraordinary level of detail, identified by the FCA, across these loans.

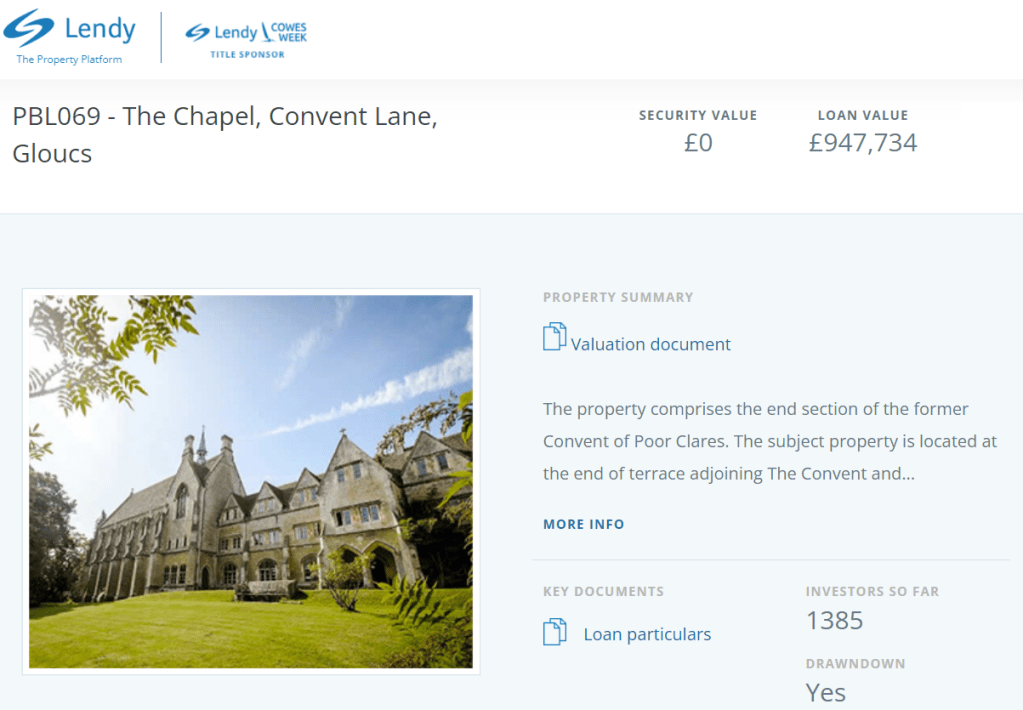

The Convent Properties — Gloucestershire

In the so-called ‘Convent Properties’ loans (circa £3.65m) displayed on the platform under references PBL069,070&071 the FCA identified that “the borrower was declared bankrupt in April 2016 but secondary market activity was allowed to continue until July 2017.” We’re told that this “information was not passed on to existing lenders or to secondary market buyers.”

“Credit checks on borrower do not appear to have been carried out until September 2016 – these show the borrower was insolvent — but no immediate action was taken to protect lenders and secondary market activity continued for a further 10 months.”

“Since April 2016 c£930,000 has been traded on the secondary market —- these buyers have not been made aware that are lending to a bankrupt borrower.”

This is a significant problem.

One of the Convent loans as displayed to users of the Lendy website

Westbury Castle, Prestatyn

In this £3.43m loan, collectively financed by some 2,361 members of the public, reference is made to a “background report dated 25 August 2017 [which was] obtained on the borrower.” The loan had commenced some 6 months earlier.

According to the FCA the report “shows the borrower has no substantive personal assets; he is known to place most property assets into SPV’s; he is ‘blacklisted’ by a number of major lenders due to historic non-performing loan portfolios.”

This again is a serious problem.

The FCA identified that “Despite the loan condition breaches, concerns on property value and the information in the background report — secondary market activity continued until 29 September 2017.”

According to the Lendy website investors only received 39.3% of their capital back when the property sold at auction in March 2018.

Campsmount, Prestbury, Cheshire

In this £1.7m loan the borrower “indicated that it was his intention to do some property alterations and use the property as his business base”. According to the FCA “no details were obtained to verify the plausibility of this.”

We are also told that “the property was sold at auction for £1.8m (compared to value of £2.45m 7 months earlier), it was sold with a tenancy that had not arranged by the borrower without Lendy’s consent.”

To continue a theme “the loan was never removed from the secondary market, even when the firm was aware that the price range at the auction could be less than the debt outstanding.”

Gateside Lodge, Stoke Poges, Slough

[Incidentally, the mouseinthecourt has attended court proceedings in this matter]

This £1.29m loan “completed in August 2016 but credit checks were not completed until 22 September 2016 and ID was not verified until a field agent visit on 20 September 2016.”

“The borrower was described to lenders as self-employed within the music industry – a subsequent background report obtained prior to the auction casts doubt on this.”

Again the “secondary market allowed to continue until August 2017 even though Lendy Ltd aware property being auctioned and the price likely to generate a significant shortfall.”

Isle of Wight care village development

This £3.25m loan had a serious problem. The FCA identified that there was a:

“number of disputes with the borrower regarding security offered, [which] has resulted in a ransom strip being transferred to the borrower’s son and access to the development site is effectively locked. The son is demanding payment of over £1m to provide access.”

Time is running out as “an appraisal report on the site suggests the current value is £1.3m and reducing as planning permission will soon expire.”

Again, running with a theme, “Secondary market activity was allowed to continue until 27 July 2017.”

Development at 17 Homer Row London

[After the date of this report this £7.1m loan generated significant litigation in the courts. Further details can be read in this judgment of Mr Justice Zacaroli]

The top concern identified by the FCA was that “This is a very complex structure and retail lenders are unlikely to be aware of exactly who they are lending to.”

We are also told that “the LTV [loan-to-value of the loan] being presented is inaccurate — as no development works had commenced the initial advance should have been assessed against the purchase price, this would then show a 77% LTV. The Secondary market is still active at present and buyers may believe they are buying a loan of 11% LTV.”

It is also revealed that “Lendy Ltd had a direct investment in this loan but subsequently sold out (date unknown)”. This is described as a “potential conflict of interest if Lendy Ltd sold their part of loan after becoming aware that the borrower had not satisfied loan conditions.”

Next steps

The FCA told the firm that “An analysis of the current loan portfolio is to be completed to assess the accuracy of information presented to lenders at the time of loan origination and to identify any instances of post-drawdown default events and/or receipt of information likely to have a material impact on the loan.”

“The firm must also provide details on how it anticipates remediating the range of cases that may be identified where there has been inaccurate or insufficient information provided to lenders at any time.”

This ultimately concluded in a ‘Review of loan file documentation’ report by insolvency experts Duff and Phelps (now Kroll). The contents of this shocking report, and the defects identified, will be revealed in subsequent reporting.

Update 04/11/2023 – The FCA have asked us to remove the name of the senior associate who wrote the letter. We have done so.

The work on this site is protected by copyright laws and treaties around the world. All such rights are reserved.

You may print off one copy, and may download extracts, of any page(s) from our site for your personal use and you may draw the attention of others within your organisation to content posted on our site.

You must not modify the paper or digital copies of any materials you have printed off or downloaded in any way, and you must not use any illustrations, photographs, video or audio sequences or any graphics separately from any accompanying text.

Our status (and that of any identified contributors) as the authors of content on our site must always be acknowledged.

You must not use any part of the content on our site for commercial purposes without obtaining a licence to do so from us or our licensors.