A trove of normally secret documents have revealed a comprehensive catalogue of missed warnings about the so-called peer-to-peer lending sector after disclosure in a recent case at the Employment Tribunal.

This substantial investigation, exclusively carried out by the mouseinthecourt, shows that for a number of years significant concerns were raised – and seemingly not acted upon – at all levels within the organisation.

The mouseinthecourt spent six days at the Employment Tribunal and countless hours researching, editing and writing. Please support crowd-funded journalism of the P2P Sector by donating to the Cheese Fund.

One e-mail, sent to the man at the top – Andrew Bailey, then CEO, said:

we are still concerned that consumers stepping in the PtP world do not know that they are potentially exposed to high risks and we believe that they cannot be expected to understand the risks even with enhanced disclosure.

7th June 2017 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight Division)

The following week an FCA Manager, citing a “lack of safeguards at the policy/advisory/access level”, wanted:

an explicit acknowledgment that we expect that retail consumers will lose some or all of their investment

12th June 2017 – E-mail sent from Natasha Pesaro – Manager (Risk & Compliance Oversight Division)

This was six-months after a different manager had said:

These are huge risk management weaknesses that we need to fix. The problem with doing that using threshold conditions is that there are billions already in this precarious state.

In the case of P2P the horse has already bolted. So we need a different strategy to manage the firms into a different place. This is not going to be easy.

29th December 2016 – Email sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Internal cognitive dissonance also appeared to run rife between the active promotion of what was a shiny new financial innovation and what was soon mooted as an unsustainable business model.

There is a disconnect that is being recognised by the platforms that what we say in public (P2P lending platforms are good, represent innovation, increase competition etc) and how we behave with respect to authorisation (we are seriously concerned about many aspects of how they operate and want change)

10th November 2016 – Internal FCA e-mail

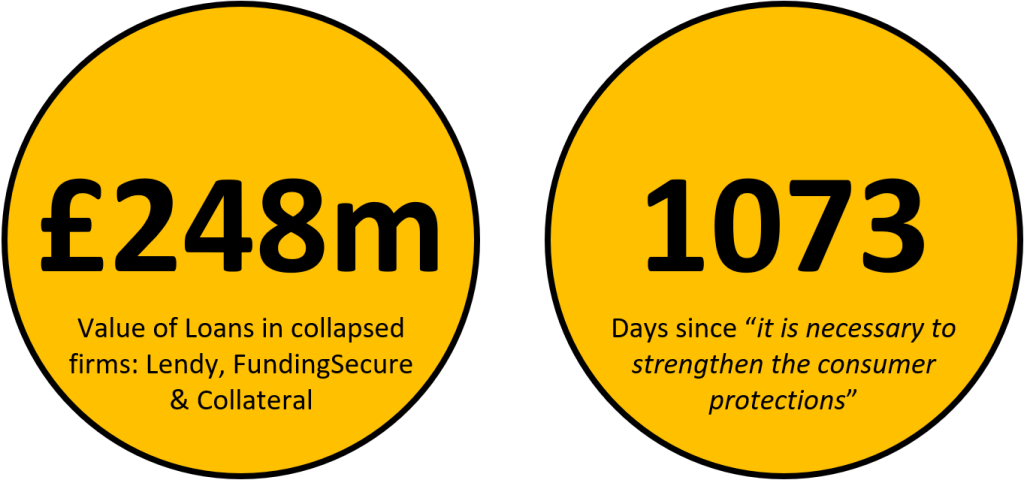

In December 2016 the Authority publicly concluded “it is necessary to strengthen the consumer protections provided by our rules” but took over 1,000 days, and the collapse of several platforms to actually do so.

Confusion over which department is responsible for what was a common theme during this period:

Overall, I would characterise where we are as:

Confused as to what we are actually trying to achieve through the regulation of P2P platforms, with different parts of the FCA with quite different short-term objectives

I still am confused about the next steps and who really makes decisions on P2P.

3rd April 2017 – E-mail sent from Jose Morago – Head of Enterprise Risk

Thousands of members of the public trusted the FCA to protect consumers like themselves. Did they achieve that objective…? Read through these explosive documents and decide for yourself.

“Financial markets need to be honest, fair and effective so consumers get a fair deal. We aim to make markets work well for individuals, for businesses and for the economy as a whole“

- The Employment Tribunal Case

- Peer-To-Peer Lending

- P2P – The good years

- And the bad years…

- LCF Bondholders

- The value of the FCA

- Revelations

- P2P & The FCA: A Timeline

- Too many cooks?

- Win a risky prize

- The FCA Board get involved

- Independence of the FCA

- If a major P2P provider implodes…

- Funding Knight goes bust

- The Executive Committee ‘EXCO’ Paper & The Concerns

- Can we refuse to authorise?

- The flaw with P2P

- What was the FCA doing in public?

- What next for investors?

- The FCA Responds

- Responses

- Writing Policy

- Case Details

The Employment Tribunal Case

Mr Walker William Sigismund was a Manager within the Risk & Compliance Oversight Division at the Financial Conduct Authority. Mr Sigismund is pursuing a claim at the Employment Tribunal that he was unfairly dismissed through redundancy after apparently blowing the whistle on a number of problems within the organisation.

Mr Sigismund says he made a series of these so-called ‘protected disclosures‘ to his bosses, one of which was that the FCA breached its legal obligation “to ensure clear fair and not misleading product information, fair pricing, and/or fair competition and market behaviours” in the peer-to-peer lending sector. The FCA denied this allegations and the tribunal has yet to hand down its judgment.

Further background about the case can be read in this Law360 article.

Peer-To-Peer Lending

Peer-to-peer (or P2P) lending is a type of finance arrangement where members of the public collectively crowdfund a loan to a borrower.

The loan can be secured against property or other assets. and the P2P platform typically acts as an agent in the transaction taking a share of the interest along with arrangement fees and the like.

P2P – The good years

The world’s first peer-to-peer loan originated in the UK in 2005 and the industry saw massive growth over the coming years. Plenty of praise was forthcoming in anticipation of what a huge opportunity this could be.

We desperately need new and innovative financial services to provide real competition for existing banks and to fund those areas of commercial life, particularly SMEs and start-ups, that the banks are so obviously failing to fund.

It is not as though innovative, real-world consumer-orientated financial services are in good supply. In fact, it could be argued that peer-to-peer lending and crowd funding are the only significant financial innovations that are around at the moment and likely to benefit the real economy.

Lord Sharkey, House of Lords 18th July 2012. Discussion on the ‘Financial Services Bill’

The industry created its own self-regulatory body, the Peer-to-Peer Finance Association, in 2011 and its then Executive Director, Ms Sam Ridler, reported that “in 2014, over £1.2bn was lent to SMEs and consumers through UK P2P platforms.”

The Government was keen to promote P2P with the then Chancellor George Osborne describing in 2014 how he wanted to “make the UK the FinTech capital of the world“.

The technologies being developed today will revolutionise the way we bank, the way we invest, the way companies raise money. It will lead to new products, new services, new lenders.

It means being able to bypass traditional banks altogether, and lend money directly – through peer-to-peer platforms like Funding Circle and Zopa, both represented here today.

My message today is simple:

We stand at the dawn of a new era in banking.

From the speech of the Rt Hon George Osborne 6th Aug 2014

The following year, in 2015, Emma Ann Hughes of the FT reported comments made by City Minister Harriett Baldwin who branded peer to peer lending as a:

…brilliantly innovative new form of finance – which we want to see continue to grow and evolve. … The businesses here – from Funding Circle to RateSetter to Zopa – are some of the most innovative in Europe.

Article: ‘Treasury sings praises of peer to peer lenders’ FT, 22nd October 2015

Do remember the platforms championed by both George Osborne and Harriett Baldwin – Funding Circle and Zopa – we’ll see how they turned out later on.

Even as late as 2018 the Government was still actively promoting P2P lending. Robert Jenrick, the then Exchequer Secretary to the Treasury told parliament that:

…using peer-to-peer lending is simply a new way of finding capital to finance working capital requirements, to fund investment in research and development, new equipment or premises, and to drive growth forward.

We believe it is an important development in financial services, and it is one we want to support…

The Rt Hon Robert Jenrick, The Exchequer Secretary to the Treasury – Speech to the House of Commons – 7th March 2018

And the bad years…

From 2019, P2P companies started to collapse amid significant financial and regulatory problems, others left the P2P environment altogether. James Hurley, Enterprise Editor at The Times, described it as the “Peer-to-peer clear out”.

Retail investors who had placed their trust in these companies, and in the system that purported to regulate them, stand to face significant losses.

A cursory inspection of peer-to-peer websites, trading forums and industry analysis quickly suggested that we had ample grounds for our concerns. Many pundits have argued for years that these systems were full of risks and so short on risk management and other safeguards that they would unravel in a downturn

28th April 2017 – Report by Walker Sigismund – Manager (Risk & Compliance Oversight) and Fod Barnes – Senior Advisor

Lendy

At its peak Lendy, a fully FCA authorised P2P company, had a loan book totalling £288m. The firm collapsed in May 2019 following eventual action by the FCA.

In a document seen by the mouseinthecourt the FCA raised concerns privately with Lendy as early as August 2016. The FCA stated that:

the issues identified at the Firm indicate to us that you may not be meeting the [FCA rules on Client Money – CASS] and we are concerned that you have not adequately considered the CASS rules and their application to your business.

12th August 2016 – Letter from the FCA to Lendy

The former directors of Lendy have since become embroiled in allegations that they misappropriated funds in excess of £6.5 million from the company during their tenure. These claims are ‘vehemently denied’ and have yet to be determined in court.

Court documents deployed by Lendy’s Joint Administrators’ in June 2021 reveal a rather damning summing-up of how this fully FCA authorised company was run:

It will be apparent … that Lendy was subject to serious mismanagement for a long period of time. The operations of Lendy were chaotic at the best of times, and investors’ funds were not properly protected or managed.

Indeed, it is surprising that Lendy managed to survive for as long as it did … the legal and contractual documentation relating to Lendy’s activities is also extremely confusing.

Written submission from the second witness statement of Damian Webb, of RSM Restructuring,

The loan book has proved to be in a significantly worse state than was immediately ascertainable on our appointment… The state of the Company’s records to comply with current [Anti-Money Laundering] regulations was unacceptable.

Progress Report to creditors dated December 2019

A four-day High Court trial was required to determine how certain contractual clauses should be construed. Lendy was found to have “acted wrongfully and with a lack of commercial probity“.

FundingSecure

FundingSecure, another fully FCA authorised P2P firm, entered administration in October 2019 with £80m of loans outstanding.

Former director and co-founder Richard Luxmore left the company after becoming caught up in allegations that he created “false and fraudulent documentation so as to conceal” payments of £8.15m whilst at the company. He denies these allegations.

Following their appointment, it became clear to the Administrators that there was a lack of clarity regarding the operation of the Platform and the Company’s client account.

Further, it was not clear, given the way that matters had been operated in practice with (amongst other things) the mixing of funds and assets, that a valid and binding trust or trusts had arisen, binding and effective against the Administrators.

Written submissions made to the High Court in the March 2021 FundingSecure directions hearing

Likewise, a High Court hearing was required to determine how certain contractual clauses should be construed.

Collateral

Collateral (UK) Limited and two related companies entered administration in April 2018. Some £16.5m was actively loaned at the date of collapse.

The FCA launched criminal proceedings against its directors in January 2022. As the matter is listed for trial it would be inappropriate to comment on anything that may be considered a live issue.

The House Crowd

In June 2020, fully FCA authorised firm ‘The House Crowd’ was placed under restrictions after what was described as “non-compliance with various regulatory rules“.

The company had been trading for nine years before entering administration in April 2021 following “concerns about THC’s viability and ability to continue to fund its operations“.

Twenty-nine loans to the tune of £15.1m were outstanding when the platform went under.

The Joint Administrators on appointment found a business that was characterised by incomplete books and accounting records; a patchwork of sometimes conflicting contractual agreements purporting to govern THC’s relationship with investors; significant cash at bank with indeterminate ownership status; and various other issues

THC Information to creditors in the Administrator’s progress report dated March 2022

The Joint Administrators’ of THC have commenced an application to the High Court which is in its early stages. Documents deployed to the court as part of an early procedural hearing suggest some 3,000 investors are affected.

Compliance with the so-called CASS rules concerning client money was something that appears to have been overlooked when the platform became fully authorised in January 2018:

THC is not authorised to hold client monies by the FCA and as such did not take steps, pre-administration, to comply with the strict provisions of CASS in relation to funds from retail lenders.

It is the Joint Administrators’ opinion (supported by legal advice) that given the nature and composition of its operations, THC should probably have formally fallen under the ambit of the FCA’s CASS rules.

22nd March 2022 – Page 13 Administrators’ Progress Report

The FCA is supportive of this view.

Zopa & Ratesetter

To put it simply – the two flagship P2P lenders lauded by George Osborne both morphed into … banks.

It once hoped to make banks a thing of the past by cutting them out of the equation, but now Zopa is shutting down its “peer-to-peer” (P2P) lending arm after 16 years – so it can concentrate on being a bank.

An article begins in The Guardian “Zopa exits peer-to-peer lending to focus on banking“

Peer-to-peer investment platform RateSetter has confirmed to customers that Metro Bank has bought its consumer loans

An Article begins on the Which.co.uk website “RateSetter to sell all loans to Metro Bank” – February 2021

ThinCats

Another platform morphed away from P2P towards an institution-only funding model for future loans. As reported in 2019 by Bridging&Commercial: “The P2P platform, operated by Business Loan Network (BLN), has now closed to new investors.“

The number of loans funded by the P2P Platform has fallen significantly over the last two years and it is no longer cost effective or practicable to raise funds in this way

Jill Sandford, chief executive at BLN, as reported by Bridging&Commercial 9th December 2019

In 2017 a Senior Associate at the FCA mused whether this may ultimately be the direction of the industry. He sent round an article entitled P2P platforms facing hybrid dilemma (from Anna Brunetti of P2P Finance News) and made the following comment:

The key argument seems to be that ‘vanilla’ p2p is not profitable enough for small P2P lenders to survive, and small-scale p2p can only be made so by moving further towards banking, investment management.

It’s interesting to see how strong the issues are around this issue.

5th June 2017 – E-mail sent from Emmanuel Schizas – Senior Associate (Crowd Funding Working Group)

LC&F Bondholders

The P2P sector is not the only section of the financial industry to have failed retail consumers. One such area – minibonds – came under the spotlight recently. In particular the matter of London Capital & Finance (LC&F).

LC&F at the date of the FCA’s eventual intervention in December 2018 had raised over £237 million from 11,625 Bondholders. Its Joint Administrators’ estimated in March 2019 that investors might only get 20% of their investment back.

In May 2019, John Glen MP directed the FCA to launch an independent investigation into the events relating to the FCA’s regulation and supervision of LC&F. This was carried out by the former Court of Appeal judge Dame Elizabeth Gloster.

John Glen MP told the House of Commons that her investigation concluded that the FCA “did not effectively supervise and regulate LCF during the relevant period”.

The Gloster Report was strongly critical of the FCA’s approach, contending that the regulator had failed to fulfil its statutory objectives and had inadequately considered issues beyond its “regulatory perimeter” or concerns raised about LC&F.

[Dame Gloster] repeatedly stressed the problem that Bailey and his top team knew the organisation needed to do more to spot fraud and wrongdoing but had failed to communicate that to the operational staff. She called that failure a “disconnect between top board level and getting that picked up to run operationally on the ground… I’m not sure why those changes took so long to implement.”

2nd February 2021 – Article “Dame Elizabeth Gloster tells MPs of “wickedness” of FCA failures to protect the public from London Capital & Finance” Jim Armitage, Evening Standard

The Government announced that the combination of circumstances was such that it would establish its own compensation scheme for LC&F bondholders – a somewhat exceptional response. Compensation was limited to a maximum of 80% of the FSCS equivalent.

The value of the FCA

Lendy was fully authorised by the FCA in July 2018. The CEO and co-founder, Mr Liam Brooke, is quoted as having said at the time:

We’re very pleased to have been given full authorisation by the FCA. It has been a long and sometimes challenging journey, which has involved a detailed review of our processes and policies and has helped us mature into a stronger and more robust business.

Statement of Liam Brooke, CEO and co-founder of Lendy, 11/07/2018

Serious questions have been raised by the members of the public who were involved in Lendy as to how the FCA came to fully authorise Lendy despite the extensive issues that are said to have existed.

Lord Myners, the former City minister, is quoted in the FT as having said that the FCA’s authorisation of Lendy gave it:

a sense of regulatory approval and endorsement, which encouraged people to feel they had been vetted … The FCA should, in my view, have been more alert.

Lord Myners, the former City minister

We spoke to an investor called Simon who says he invested £450,000 in crowd-funded loans facilitated by Lendy and that he…

saw the FCA as a rubber stamp that the business was being run honestly and correctly, and thus was assured it wasn’t a scam. I would not have invested anything without the FCA involvement. All this turned out to be rubbish, hence we are where we are!

Lendy investor ‘Simon’

The regulatory journey of Lendy was featured within the True and Fair Campaign report ‘Asleep at the Wheel‘. Self-styled as “An exposé of systemic regulatory failure and consumer detriment in the UK financial services sector” it suggests that the full authorisation of the company “gave investors, who were unaware of what was going on with the business, the confidence to lend“.

Revelations

Some 16,000 pages of Employment Tribunal documents have been combed through and reveal a damning culture of confusion and complacency at the FCA when it came to the regulation of the peer-to-peer lending sector. Warnings were missed and mitigation was slow to be implemented.

From what we’ve seen, managers and department heads did not know who should be responsible for what. Repeatedly, risks were downplayed or removed from documents shown to the FCA Board and in an FCA Manager’s own words the authority was “reactive, with little will to become proactive“.

You may well conclude that hundreds of thousands of members of the public have been failed by a system that was slow to react and reluctant to take responsibility.

P2P & The FCA: A Timeline

Some of the key lines taken from the documents presented to the tribunal:

P2P has “substantially more risk passing to consumers along with much lower professional risk management”

April 2016“the risk of complete capital loss to consumers”

April 2016“the market is not working on its own to create a safe space for consumers and standard setting bodies and legislatures need to seriously consider how to prevent this becoming a systemic risk”

June 2016“the FCA does not have a very deep understanding of the financial and economic consequences of these new business models”

June 2016“this is a matter of public confidence and execution risk … However, when things go wrong the FCA will be held responsible first and foremost”

July 2016“should/when some of the financial risks currently held by lenders/investors crystallize it will look – particularly in retrospect – that customers were not being given an adequate level of consumer protection”

July 2016“We therefore see this area of ‘innovation’ as very risky to our objectives and reputation.”

Aug 2016“we feel/have reason to believe that the risk in the sector is increasing and they are becoming more urgent”

Sept 2016[Risk & Compliance Oversight] “sample checks which pointed to a large proportion of assets being subprime”

October 2016“there are almost no safeguards at firm, market and regulatory level”

November 2016“it is increasingly clear that the risks in P2P are much greater than those in banks, asset managers and securitisation; so much so that those areas would likely fail with comparable risk levels”

November 2016“There is agreement that the quality of the credit checking could be a serious issue”

November 2016“The p2p market does not appear viable to borrowers.”

December 2016“The industry does not fully appreciate the problems it has fostered, especially the impact on consumers and markets… This appears to be a PPI like dilemma, whether it is will of course throw a huge spanner in the works.”

December 2016“These are huge risk management weaknesses that we need to fix … there are billions already in this precarious state.”

December 2016“we all agree that PtP often does not provide a good proposition to both borrowers and retail investors, but the bar for rejecting applications is too high … Legal basically advises against rejecting any of them given that we cannot substantiate that the business models are not sustainable”

January 2017“the p2p loans systems are not meeting our objectives and need to be substantially transformed to do so”

February 2017“P2P is inherently very inefficient and uncompetitive when it comes to managing complex loan system risks”

February 2017“The P2P model hides losses for long periods and then suddenly breaks without warning to investors or regulators”

May 2017“it appears that retail investors can be exposed to significant lending risks…we are dealing with a long fault line running through p2p, not just a small issue in an isolated situation.”

May 2017“we are still concerned that consumers stepping in the PtP world do not know that they are potentially exposed to high risks”

June 2017“if there were some form of access restriction (e.g. retail investment limits), or an explicit acknowledgment that we expect that retail consumers will lose some or all of their investment, then we would no longer need to apply that significant level of regulatory scrutiny”

June 2017“the much bigger problem is that the harm to retail investors, the retail lenders who put their money in a scheme that is opaque and high risk”

June 2017“We feel that the priority need is for FCA to press ‘re-set’ on the P2P landscape – our regulatory expectations, firms’ obligations, and consumers’ rights”

June 2017“we are assuming the [Executive Committee] etc can immediately deal with the complexity of the issues and come up with the right approach. History ███████ tells something different.”

November 2017“we should be taking action under our current regime but we are not. Somehow the FCA keeps turning away from this uncomfortable fact. We need to do more to figure out (a) why we keep hiding from these facts and our rules”

November 2017“is it possible to design a p2p system which meets FCA objectives (ie does not cause harm)…The current system is nowhere close on the evidence we have to hand”

November 2017“With a better process for looking ahead, and more deeply into the risks, the FCA might have had regard for p2p problems from the beginning.”

July 2018

Too many cooks?

A senior associate of mortgage policy sent this e-mail around, it seems many plates had been spinning at the FCA with no overall coordination:

I am putting together details of the various work streams that are currently taking place within the organisation on Crowdfunding/P2P. If you are working on any such project/review can you let me have high level details (eg scope) together with timescales.

6th April 2016 – E-mail sent from [“UF”] – Senior Associate (Mortgage policy)

She receives a response from Walker Sigismund who raises concerns:

Dear [“UF”],

The Risk and Compliance Division has been interested in p2p for some time as an example of a cross cutting risk that may not be fully appreciated by our normal way of looking at things.We note that the economic function is very similar to banks, funds and securitisation but with substantially more risk passing to consumers along with much lower professional risk management, balance sheet buffers, market pricing, clean data and regulation to protect them.

We have proposed that our Director Barbara Frohn flag these issues in a quarterly ESRC [Economic and Social Research Council] update paper.

7th April 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Walker

Mr Sigismund was keen to push this further and sent another e-mail the following day:

I am still unsure who is writing the proposed [Executive Regulatory Issues Committee] paper, so if anyone knows please let us know.

Meanwhile, as many of you know from correspondence or discussions, the risk department has been investigating a number of issues around p2p that, given many of you are doing the same, we thought best to share more broadly in the hope that it might prove useful.

In general we have focused on comparing the consumer and market outcomes of p2p with other financial functions. We note that the economic function is very similar to banks, funds and securitisation but with substantially more risk passing to consumers along with much lower professional risk management, balance sheet buffers, market pricing, clean data and regulation to protect them. So the big question is to determine the impact of those differences in both qualitative and quantitative ways, both of which the enclosed note outlines.

We have proposed that our Director Barbara Frohn flag these issues in a quarterly [Economic and Social Research Council] update paper as an example of a cross-cutting risk that does not fit well within any individual area but could add up to be quite significant for consumers and market integrity.

8th April 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Andrew Kay, a Manager in the Consumer Credit Department, replied:

We have been asked by Jonathan Davidson to “…prepare a Sector Evaluation document to highlight the risks presented by the sector and to set out what Supervisory strategy and other tools might be appropriate and hold a Sector Evaluation Meeting to agree the way forward.”

I think there’s a considerable risk here (which Walker is calling out, and we’re all conscious of) that we’re all working on separate briefs and papers to the same end and that, across the organisation, we are busily documenting/updating similar risks in different formats to satisfy those briefs.

It would be useful to co-ordinate our interests by agreeing a single ‘house view’ of the crowdfunding/P2P sector (and associated risks) and to fully understand what work each area is taking forward

8th April 2016 – E-mail sent from Andrew Kay – Manager (Consumer Credit Department)

David Tait adds to this e-mail chain and explained what his department is doing. A “risk of complete capital loss to consumers” is considered.

Following on from Andrew’s email, Retail Investments supervision and financial promotions are undertaking a piece of multi-firm work considering the due diligence, disclosure and promotions of 5 investment-based crowdfunding platforms █████████████ ████████████████████. The work is currently underway and should conclude by early May.

The work will test whether the platforms have determined the risks present in their business models and have developed appropriate processes to mitigate them to ensure that investors have all the information they need to be able to make informed investment decisions and that all communications are fair, clear and not misleading.

Given the disclosure based regime, the risk of complete capital loss to consumers and previous financial promotion failings, supervision and financial promotions have requested the firms provide details of their systems and controls in relation to each of the following areas:

– Overview of business model

– Appropriateness details

– Legal Due Diligence

– Financial Due Diligence

– Corporate Review and Shareholder Rights

– AML and KYC

– Remuneration

– Conflicts of Interest

– Financial Promotion Controls

– Investment Pitch MonitoringUsing the information gathered, supervision and financial promotions will request 3 investment pitches from each platform which will then be reviewed for compliance with the financial promotion rules and requirements, as well as each firms own processes.

8th April 2016 – E-mail sent from David Tait – Manager (Investment Intermediaries & Scams Department)

Walker considered whether these risks would actually be recognised within the Authority:

Fod and I consider that such rules can and must be done mostly in house and cannot be achieved via the normal practice of expecting the industry to propose appropriate safeguards. The industry does not fully appreciate the problems it has fostered, especially the impact on consumers and markets.

This appears to be a PPI like dilemma, whether it is will of course throw a huge spanner in the works.

22nd December 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Win a risky prize

Meanwhile, a senior manager had sent out an e-mail to generate ideas:

Time to put your thinking caps on.

Barbara is very keen to have your input on the regulatory risks that are keeping you awake.

Please send me your top three lis (sic), with a brief description of each risk by Monday.

There are mystery prizes for the most insightful suggestions – anyone can enter

7th April 2016 – E-mail sent from Dr Azhar Rizvi – Senior Manager (Group Risk)

Walker Sigismund replied…

Az,

I try not to let risks keep me up at night, but the things that seem biggest to me are several structural changes that are underway like the following:

Risk pushed onto consumers rather than caught by professional risk managers, balance sheet buffers, and other regulations. There is a general trend for professionals to merely charge fees and push almost all risks onto consumers as a smorgasbord of products and services to choose from, increasingly using apps. This makes them very accessible, but does not make the risk that much easier to access or manage.

P2p would be an example, as would other forms of shadow banking…..

Given the way the FCA is organised supervision, sectors and policy areas are unlikely to fully analyse and recognise the probable consumer detriment and market integrity issues in this trend; indeed since the risk is lower in firms and sectors the might even see it as a positive. So an organisational change to capture and evaluate this sort of ‘pushed-out’ risk is probably needed.

11th April 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

The FCA Board get involved

The FCA Board has an important job – it “keeps a close watch on how [The FCA] is operating and holds [The FCA] accountable for the way they work. It is made up of executive and non-executive members.”

The e-mails reveal that a report was presented to them, again concerns were raised:

We took the attached slides and paper to the Board this afternoon.

The Board said:

They are concerned about the evolution of the P2P sector and the potential for detriment to investors, particularly ordinary retail investors who regard the ISA brand as relatively secure

They would like us to conduct an in-depth post-implementation review of the P2P regime and consider tightening the rules.

In the meantime, they would like a particular focus on P2P fin proms, particularly concerning P2P ISAs

Before we authorise the ████████ platforms (████████) we should publish a discussion paper that:

– Sets out our concerns at a High level

– Suggests areas where we may wish to change our rules

– Invites feedbackWe should then undertake the thematic review and other research and publish a consultation paper with appropriate new rules in due course.

Jonathan Davidson is due to meet HMT [Her Majesty’s Treasury] to discuss the Board’s concerns with the market and signal our next steps.

26th May 2016 – E-mail sent from [“QS”] – Technical Specialist

We can cross-check this private version with these public minutes published on-line:

5.2 Peer to Peer Lending regulation

The Board received the paper and noted the background to the regulation of Peer to Peer lending since 2014, the developments in the market and the challenges for the current regulatory approach and how it compared to regulation for other activities.The Board discussed the changes in the market and the possible alternatives to the current disclosure based regime, noting that the Executive were not yet in a position to provide a considered view to the Board on this prior to carrying out a post implementation review.

The Board supported the work to carry out a review. The Board noted the potential benefits to competition and also the need to ensure that consumers continued to be protected appropriately. It encouraged the Executive to communicate that the FCA was looking closely at this area.

FCA Board Minutes 25th and 26th May 2016

Quite the contrast between what was said in public “consumers continued to be protected” and what was said in private “concerned about the evolution of the P2P sector and the potential for detriment to investors“. Sentiments also echoed in this e-mail sent a few months later:

…there is a disconnect that is being recognised by the platforms that what we say in public (P2P lending platforms are good, represent innovation, increase competition etc) and how we behave with respect to authorisation (we are seriously concerned about many aspects of how they operate and want change)…

10th November 2016 – Internal FCA e-mail

Independence of the FCA

The purported independence of the FCA is explained well in comments made by the City Minister and Economic Secretary to the Treasury John Glen MP:

Although the Treasury sets the legal framework for the regulation of financial services, it has strictly limited powers in relation to the FCA. In particular, the Treasury has no general power of direction over the FCA and cannot intervene in individual cases.

The independence of the FCA is vital to its role. Its credibility, authority and value to consumers would be undermined if it were possible for the Government to intervene in its decision-making.

17th March 2022 – E-Mail sent from John Glen MP, in his role as City Minister and Economic Secretary to the Treasury

Let us consider whether this is actually the case by reading this e-mail:

Andrew Bailey was at the Board discussion and commented that the FCA would take any blame if this goes wrong; his position is not entirely transparent but was aligned with the Board outcome.

The idea would for all that to conclude by February 2017 in time for the next ISA season. These are tight deadlines given that many of our concerns are still in formative stages and one can expect substantial pushback.

David Geale and ____ will be meeting Treasury shortly to let them know a discussion and consultation paper is in the works.

This would give GO time to write to tell us not to do it.

1st June 2016 – E-mail sent from Walker Sigismund – Manager (Risk and Compliance Oversight)

If it is true that ‘substantial pushback’ was expected from the treasury, and if it is true that “GO” stands for George Osborne, then this is an e-mail which blows apart the comments made by John Glen MP as to the independence of the organisation.

Further apparent political intervention was revealed in an e-mail sent the following day:

What has driven this change? Apparently our Chairman has had several MP’s corner him, and bank NEDs [Non-Executive Directors] have been asking why these shadow firms were subject to a much lighter regulatory regime. The treasury drive to carve out easier rules in the P2P space has also raised the concerns with the TSC [Treasury Select Committee] and Andrew Tyrie as we see here.

2nd June 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

And in a report the following month:

The Treasury appear to be moving the boundary quite frequently, which doesn’t help.

27th July 2016 – A report ‘Breaking down the authorisation problem’ authored by Fod Barnes – Senior Advisor

The tricky situation the FCA is in is discussed in an Executive Committee paper the following year. Was it simply more convenient to do nothing?

5.1 Introducing more detailed rules could be criticised as hindering innovation, and any consequential failure of platforms to raise funds or attract new clients (both investors and borrowers) may be attributed to our proposals.

5.2 Some parts of the industry have called for us to supervise more robustly against the existing rules, therefore consulting on additional rules could be criticised.

13th June 2017 – ExCo paper ‘Crowdfunding post implementation review – Consultation on new rules and next steps’ Sponsor – Christopher Woolard

If a major P2P provider implodes…

The risk of contagion within the sector is considered in this e-mail:

If a major P2P provider implodes or a number of smaller players fail then there is an integrity issue for the sector and for “alternative finance” in general. Likewise, the FCA is likely to be closely scrutinised for “allowing” the “poster-boy” of alternative finance to fail/hurt consumers/Kill the dream.

2nd November 2016 – E-mail sent from [“DN”]- Technical Specialist, (CEO’s Office)

Contagion isn’t the only risk when a platform fails – how investors funds are recovered, and who pays for that recovery has been an issue in recent platform failures … an issue that was anticipated:

The recovery and resolution angle: in case of problems of the platform, third parties may not be able or unwilling to take over servicing. We are not convinced that the disentanglement of payment flows is something third parties will find attractive or feasible. Consumer detriment is the result.

5th January 2017 – E-mail sent from Barbara Frohn – Director (Risk and Compliance Oversight)

Particularly as…

The P2P model hides losses for long period and then suddenly breaks without warning to investors or regulators

26th May 2017 – R&CO Analysis Report

At least four-and-a-half years later the problem still existed:

Our recent supervisory work leaves us generally dissatisfied with the WDPs [wind down plans] that we have reviewed.

All had assumed a voluntary wind-down, and none had adequately identified the triggers that might realistically allow for a solvent wind-down to be invoked. Coupled with a lack of liquidity monitoring and capital adequacy planning, we found little evidence of firms’ ability to identify when an invocation of their wind-down plan would realistically ensure an orderly winddown.

25th May 2021 – ‘Dear Board of Directors’ letter sent by the FCA

Funding Knight goes bust

In July 2016, the website thisismoney.co.uk, reported that a “peer-to-peer investing website that holds the cash of 900 savers has gone into administration after running out of money.”

The link to this story was sent internally within the FCA:

FYI something to watch.

We have had some concerns for some time about some of the PtP business models in the risk division.

7th July 2016 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight)

Walker responded:

Realistically the FCA needs to analyse their financial and economic interests or pay for a really good set of consultants to do so (since we do not appear to have this capacity)

11th July 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

A subsequent e-mail said:

Sigh. That looks really bad. None of our messages seems to have taken on board. I will add to the worry list for AB.

11th July 2016 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight)

Thanks a lot for that

The Executive Committee ‘EXCO’ Paper & The Concerns

Contained within the trove of e-mails were various to-ing’s and fro-ing’s of how best to relay concerns over P2P.

On June 1st 2016 Walker Sigismund explained the next steps on the ‘discussion paper’ that had been requested by the FCA board:

Just met with [“QS”] [FCA Technical Specialist] to get his view on the next ‘Peer-to-Peer’ steps.

We have the draft EXCO [Executive Committee] paper which is on a tight turnaround as it will go to EXCO and back to the Board within weeks.

[“QS”] is starting work on a Discussion paper for publication in weeks, which would lead into a Consultation Paper later in the year.

The idea would for all that to conclude by February 2017 in time for the next ISA season. These are tight deadlines given that many of our concerns are still in formative stages and one can expect substantial pushback.

David Geale and ____ will be meeting Treasury shortly to let them know a discussion and consultation paper is in the works.

1st June 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Walker Sigismund set out his concerns in greater detail the following day. He explained that concerns were raised in a slide but only some of them had been presented:

I have been trying to figure out what things [Risk and Compliance Oversight] should be most worried about in this P2P (market based finance) space given all the recent changes including this note from Tyrie, and then suggest our next steps.

A couple of months ago we suggested several slides for an ERIC [Executive Regulatory Issues Committee] paper flagging our concerns that:

(a) there were big unrecognised risks in this space and

(b) very different regulatory and consumer protections in the P2P compared to traditional spaces.

As a result we suggested that the FCA should reconsider its drive to manage through the authorisation of these firms without first making sure it was on top of these issues. At the time P2P was considered so small that it was undeserving of much supervisory resource; the list of CRM risks was short and just covered things like CASS rules being followed or the platforms obtaining the right permissions. Instead we suggested the underlying issues requires policy to fully reconsider the risks and suitability of our rules in this area.

Although those ERIC [Executive Regulatory Issues Committee] slides were not presented-apart perhaps from Fod’s note on agency and principle risk in this space-at this point our prior concerns now seem to be fully accepted and the general course of action appears on track. For example besides the discussion papers and policy rethink, ESB reports this morning that authorisation are ████████. So we have the outcome we sought.

What has driven this change? Apparently our Chairman has had several MP’s corner him, and bank NEDs have been asking why these shadow firms were subject to a much lighter regulatory regime. The treasury drive to carve out easier rules in the P2P space has also raised the concerns with the TSC and Andrew Tyrie as we see here. ████████.

By looking hard one can also find good commentary – for example the paper that I used to explain how normal firms are capturing P2P through the back door- also make it clear that the industry has evolved over the last couple years in a totally non peer to peer way resulting in substantial market integrity issues.

Finally ████████ it is unclear whether market participants can see through these very complex markets and business models to properly and really assess the risks. If they cannot, then it follows that the market is not working on its own to create a safe space for consumers and standard setting bodies and legislatures need to seriously consider how to prevent this becoming a systemic risk.

Given all that, R&CO should be broadly satisfied that the problem is now squarely on the table for discussion and action, but can we be satisfied that the FCA is prepared to grasp the bull by the horns? And find the right way to do that?

I believe that the nub of R&CO concern should be that the FCA does not have a very deep understanding of the financial and economic consequences of these new business models and many of the approaches we use are not designed to unpick them. Without that good policy is hard to achieve.

… In essence CED and the FCA need to test the viability of specific features which are (or are not) in specific platforms and who takes the risk? Originally and in general, the platforms provides services for a fee and pass all risk directly onto consumers; but increasingly they are adding features which moderate that so that some of the risk is taken by outsiders or shared across the platform. These risks go far beyond the CRM risks currently flagged. The FSB principles and recommendations need to be adhered to here.

2nd June 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Walker Sigismund sent further concerns via e-mail over the coming days:

Proposed P2P Authorisations Risk Framework version 6A

Consumer Lenders need to be very sophisticated

Peer to peer platforms pass most of the risk onto lenders. The credit evaluation of borrowers by the platform and the ability and skill of investors to verify and test this evaluation is therefore a critical element of the authorisation process and operational restrictions. This starts with an evaluation of the vulnerability of borrowers and their ability to repay loans; this needs to be thoroughly understood and tested in the authorisation process.

22nd July 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Proposed Authorisations RiskCo P2P Risk Box Version 4a

Co-Ordinated by Walker Sigismund, July 21 2016

Besides getting the right outcome for the circumstances, this is a matter of public confidence and execution risk. Managing this arbitrage is hampered by the political intention of encouraging p2p carve-outs via article 36H.

However, when things go wrong the FCA will be held responsible first and foremost, se we need to have the best possible information and analysis to get this right. To build policies, authorisation thresholds and ongoing regulatory criteria… and explain our actions to stakeholders, we need a risk management approach which is as sophisticated and deep as the underlying complex activities.

25th July 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

A report ‘Breaking down the authorisation problem’ is sent out by Fod Barnes (Senior Advisor) two days later. He identified some serious risks:

The Treasury appear to be moving the boundary quite frequently, which doesn’t help. However, wherever the Treasury put the boundary one or more of the FCA’s problems listed below would seem to be current:

A. Some firms with interim permission appear to be operating some or all of their operations such that they are currently outside the P2P boundary (do not meet their H36 conditions in the jargon).

B. Some firms that are inside the P2P boundary are doing things that do not meet the general requirements of P2P authorisation (but could quite easily do so)

C. Some firms that are inside the P2P boundary, and are conforming to the rules, are doing things where the rules applying to P2P operation do not seem to be adequate given the precise activities of the platform/firm.

This creates a risk to the FCA’s objectives (e.g. something like: should/when some of the financial risks currently held by lenders/investors crystallize it will look – particularly in retrospect – that customers were not being given an adequate level of consumer protection)

In summary, what is needed is to develop the policy of what the rules should be as we move through the complexity/diversity of what the platform is selling to customers. (Characterised by the complexity of what is being sold, rather than the complexity of the business model – as the business model may be quite simple – take an agent’s % of all transactions across any platform.)

27th July 2016 – Report ‘Breaking down the authorisation problem’ authored by Fod Barnes

Authorisations are discussed a week later in an e-mail from Walker Sigismund:

Another aim would be to address the real issues in the p2p pipeline from all the relevant perspectives. You suggested that we need to recognise where we are, pragmatically try to triage firms in the authorisation pipeline into those that need intensive work (perhaps ████████) and those that can be let through where some work might need to continue on the inside of the perimeter.

I was also struck (and Fod and I agree) by your comment that the main issues are not to do with consumer credit (where these problems are lodged) but more on whether the investor is going to get their money back as much as expected.

To see these ‘future’ problems today the FCA needs to use more sophisticated business model analysis (to figure out what is going on inside the complex black boxes) and develop policies that result from that analysis.

3rd August 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

More warning are sent later that same month:

In the last couple months R&CO have reviewed earlier drafts of this paper, closely examined the economic characteristics and risks of one of the complex p2p cases (████████), and had extensive discussions with the authorisations managers about the issues outlined in this paper.

This paper excellently presents a wide range of complex business models in the pipeline and the risks they pose. The more complex applications have many features in common with banks and securitisation waterfalls, but with few of the balance sheet, disclosure, due diligence, risk management, regulatory and consumer safeguards. We therefore see this area of ‘innovation’ as very risky to our objectives and reputation.

Besides commending the excellent description of the issues found in the paper, R&CO would like to emphasize the following:

– The simplest vanilla p2p loan is high risk because the lender is exposed to the collapse of a single loan. This can be partially mitigated through diversification, and a number of UK platforms essentially provide an automatic diversification process by parcelling out the lenders money across a number of similar borrowers, however, if the initial underwriting take-on / evaluation of the desired customer is flawed or open to a low-side override, then this exacerbates the likelihood of an increased and possibly unsustainable default level across the overall portfolio…

The FCA really needs to establish what (in terms of consumer outcomes on both sides of the platform) it is trying to achieve through regulation. (Or, in the negative, what the FCA is trying to stop happening.)

– When compared to other innovative areas (for example Simple Transparent and Standardised securitisations) where a great deal of effort has been expanded to define a market which meets our objectives, it is striking that the p2p market has features which the STS market has proscribed. This makes thep2p (sic) market appear more risky, even before any adjustment is made for the less financially capable participants.

R&CO appreciates the case made in the paper that the broader issues go beyond supervision. Indeed many of the impediments from clearing the pipeline stem from the fact that the broader consumer, economic, policy and political issues are not sufficiently developed in the FCA to handle the actual cases in the pipeline. 1 R&CO recommends that the FCA improves the coordination of the cross-cutting issues and makes sure that they meet the benchmarks set out above and in our objective.

31st August 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Fod Barnes (Senior Advisor) also sent round his concerns:

A material distinguishing feature of the P2P retail lending markets is that the retail lender directly takes on the default risk of the borrower(s) that the lender has lent to, through the platform. For such a market to work well the lender either has to conduct an adequate credit check on the borrower(s), or the lender’s agent has to do so. In general (in the UK) it is the lender’s agent that does this, which may be the platform or it may be a related entity. This immediately creates a principle/agent issue, and the market is unlikely to work well unless the lenders have sufficient information to effectively monitor their agents and/or regulation constrains their behaviour.

The developments in the operation of P2P platforms and, more importantly, the management of the network of lending/borrowing relationships has, or is potentially, making it much harder for lenders to monitor the behaviour of that management and, therefore, making sure that:

The agent is doing a good job of checking the credit worthiness of borrowers, and pricing the loan (to the borrower) appropriately

The agent is providing sufficient information to the lender as to the risk they are actually taking in lending through the platform, so that the lender can decide if they want to take the risk, for the potential reward on offer.

In addition the market for both platform services and the resulting network of lending/borrowing relationships has, or appears to be developing, the following characteristics.

– The network of lending and borrowing may not “run-off” smoothly even if the administration of the platform itself can be easily transferred should a platform fail. This can arise when lenders in the network have shorter maturity than borrowers. It is also possible that a network could need to be run down without the trigger being the failure of the platform. It is not obvious that this is always possible, given the maturity transformation that is taking place.

– Default rates appear to be rising ████████████

– Very high risk borrowers are being serviced ████████████

– The precise legal form of the platform / network appears to drive regulatory controls, rather than the economic characteristics of the services being sold ████████████

Evidence is emerging from around the world, and to a lessor extent from the UK, that the potential risks identified above are starting to crystallise in the P2P markets. Although the UK markets are not necessarily the same as other P2P markets the underlying economic characteristics are likely to be very similar, with similar commercial and other pressures applying to the platforms and other institutions.

Hoping that the UK industry will behaving differently, without strong evidence that this is the case, would seem to be a very high-risk strategy for a regulator.

26th September 2016 – E-mail sent from Fod Barnes – Senior Advisor

[“HC”], the private secretary to Barbara Frohn (Director of Risk & Compliance Oversight) gets involved with the Risk Box. He has reworded it and is “conscious that I have removed a lot of the issues which Walker raised in his draft“.

Hi all,

I have just had a chat with Walker on this, and I wanted to check in with you all. Both Walker and I agree that regardless of whether we send a risk box today, or not, to David Geale [Director of Policy], it would be good for someone (Barbara if she is back) to meet with David next week to discuss some of our concerns about the sector and the FCA’s approach.

If we think it is useful to send a risk box today, I have had a go at rewording Walkers earlier risk box (see full draft in red below). I am conscious that I have removed a lot of the issues which Walker raised in his draft; but what I am trying to say is the following:

1. Say that we feel/have reason to believe that the risk in the sector is increasing and they are becoming more urgent

2. Given this the FCA may want to consider a different approach

3. That approach could include setting up a team to a) assess the risks more sufficiently; and b) start producing policy to target the risks.

Given this is an important topic for Barbara I am still unsure whether the draft below is enough/right, so we may want to just arrange a meeting with David to a) buy us more time to engage with Barbara; and b) to ensure this lands and achieves the outcome we are seeking to achieve.

Welcome any views… ..

Thanks

[“HC”]

The paper sets out in detail some of the key issues and risks to our objectives posed by the crowd funding sector. R&CO is supportive further policy action to mitigate the risk of consumer detriment to investors in the crowd-funding sector. However, it is R&CO have reason to believe that the risks posed to the FCA’s objectives by this market may be increasing; and that quite a high proportion of the issues set out in the paper are becoming more urgent. Given this, the FCA may want to consider whether it can start further work on assessing and addressing the key issues and risks in this sector sooner than proposed in the paper.

To do this we propose that the FCA considers creating a small working group, or team (including Policy, Supervision and Authorisations personnel) to carry out the following work:

i) Analyse the information which is currently available externally and internally, including information from firms which have been through, or are in, the authorisations process, to further asses and measure the level of risk to our objectives in this sector; and

ii) Where relevant produce targeted policy proposals to ensure we have appropriately rules and regulations in place for this sector.

Risk & Compliance Oversight would be open to providing resource for this working group or team.

23rd September 2016 – E-mail sent from [“HC”] – Private Secretary to Barbara Frohn

This is not the only time that Mr Sigismund’s risk box warnings are edited:

Dear all,

Following comments from Chris Woolard on the draft ExCo paper, I have updated it to improve the messaging and structure. While much of it remains the same as the last version you saw (but in a new structure), the tone is a little different and there is now a proposal that we publish a feedback statement to the call for input, before Christmas, setting out plans for ongoing work and consultation next year. This will help alert firms to our concerns.

5th October 2016 – E-mail sent from [“QS”] – Technical Specialist

Mr Sigismund seemed unhappy about the changes:

The ‘Policy’ Paper has been roughly cut in half – removing most of the evidence and analysis – and reoriented to claim there is no evidence or analysis to suggest there is a problem or reason to do anything special before the next ISA season.

There are two dangerous waterfalls ahead where new policy and principles are required.

The first is those needed to authorise (or not) the firms. The second is the upcoming ISA season, for those authorised. If the FCA goes down either of these without a much more complete policy built around currently available data and analysis (of the sort removed that needed better explanation not less) then it will be much harder to fix.

That is why I think authorisations are going to present a very different picture. The data that is needed is already mostly to hand, it just needs to be analysed. The urgency is the need to prevent an accident over those two tricky imminent waterfalls.

Hopefully their paper will make this much more clear and then the disconnect between the two will be more evident.

6th October 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Barbara added her comments on the underlying draft Risk Box:

Comments:

– Footnote 1 indicates that 18% of people perceive the risk as low and 19% are unable to assess it. This contrasts with R&CO sample checks which pointed to a large proportion of assets being subprime.

– 3.3 while we agree that these are major risks, there are more than those listed in 3.3.

– Misleading information:

– default funds leading to a false sense of security

– default rates not reflecting commonly used (Basel) default definition leading to a flattened rate

– no publication of loss rates

– difficult to navigate internet sites, esp. on risk related information

– No skin the game for platform executives potentially leading to low investment in robust risk management. Indications that risk management is less than robust

…

3.7 While we agree that there may not be enough justification to using the temporary product intervention rule-making power, there is circumstantial evidence and real evidence gathered by Authorisations that is staring us in the face.

Concerning is that:

– We are lagging behind peer regulators

– We cannot be seen to be dragging our feet

We should therefore, in the interim period, use the powers that we do have:

– While emphasising the importance of access to finance and innovation, issue a strong message that there are areas of concern in CF and PtP that we will tackle.

– Financial promotions to use their existing powers to structurally manage cases of misleading information. [Risk and Compliance Oversight] can support this effort.

6th October 2016 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight)

A similar discussion took place between Walker Sigismund and [“DN”] a few weeks later. We’re told that despite the issues identified “we would need to see if [they are] more compelling politically than continuing to act as cheerleader for the sector“:

But to extend this to say that P2P is as small or smaller than activities we ignore in established areas is a fallacy. The reasons are that

3rd November 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

(1) there are almost no safeguards at firm, market and regulatory level and

(2) we do not even know whether the risks it generates is within our risk appetite.

For example it is increasingly clear that the risks in P2P are much greater than those in banks, asset managers and securitisation; so much so that those areas would likely fail with comparable risk levels and/or we would immediately put all hands to the pump to prevent or deal with such outcomes.

Walker

I think we are agreeing. I think the key is to be able to quantify/qualify the following in a manner that makes it comparable to how the FCA thinks about more familiar sectors

…it is increasingly clear that the risks in P2P are much greater that those in banks, asset managers and securitisation.

So, can we:

– put a number on potential consumer detriment

– qualify the potential market integrity (contagion) risk

– qualify the potential public confidence risk (to FCA)

– determine the velocity of those risks (how soon to crystallisation)

– determine root causes/market conditions and the interventions that bring these risks within a tolerance, or alternatively whether/how we can accept the risks (i.e. let them crash)Of course, then we would need to see if the above is more compelling politically than continuing to act as cheerleader for the sector

Regards

[“DN”]

3rd November 2016 – E-mail sent from [“DN”] – Technical Specialist (CEO’s Office)

Reactive rather than proactive? Walker Sigismund’s responded to the above:

The problem with our risk appetite is that it never tests such bias and assumption, because no time is spent until it is big… That is the problem here.

3rd November 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

In November 2016 an e-mail is sent out revealing that staff seem nervous about the reaction of their managers to some of the concerns raised. What does this say about the culture at the FCA?

In addition there is a rather delicate issue of a draft letter that the Board wants Andrew to send to the Treasury which we are trying to influence, but we are under strict instructions NOT to share or discuss it above working level.

There is agreement that the quality of the credit checking could be a serious issue…

However, this progress may be fragile and participants seem nervous about the reaction of their managers to this, as it acknowledges significant problems (without off the shelf solutions) that need to be addressed on a different timeline and priority than currently envisioned.

Overall, I would characterise where we are as:

1. Confused as to what we are actually trying to achieve through the regulation of P2P platforms, with different parts of the FCA with quite different short-term objectives2. Being reactive, with little will to become proactive.

3. In a negative spiral of “we won’t/can’t act/no point in developing good policy/no point in acting because policy/rules don’t work”

….

There are a number of issues that have come to light in the analysis of where we have got to on P2P platforms. In brief, these are:

1 – a number of platforms operating under Interim Permissions are not in conformity with the “rules” as they are currently articulated. ███████.

2 – the path from where they are now to where they would need to be compliant with the existing rules is not straightforward, but the FCA has not really addressed the problem of actually how to allow the transition in a way that protects (as far as possible) our objectives. And, importantly;

3 – there appears to be some confusion amongst the platforms as to what the rules actually are in practice, and the FCA does not seem to have a coherent and consistent view as to whether the platforms do fully understand the existing rules. ██████████

4 – the complete rule set facing a platform is actually quite confusing….

5 – there is a disconnect that is being recognised by the platforms that what we say in public (P2P lending platforms are good, represent innovation, increase competition etc) and how we behave with respect to authorisation (we are seriously concerned about many aspects of how they operate and want change)

…

8 – there are some other, more minor, issues as well (such as contract changes being imposed on customers without any choice and constantly changing product/service specifications of what the platforms are supplying to their customers) which the FCA is likely to have to address at some point, even if it is only to confirm that such behaviour lies within the boundary of treating customers fairly.

10th November 2016 – Fod Barnes – Senior Advisor & Walker Sigismund – Manager (Risk & Compliance Oversight)

A few weeks later we hear that Barbara and Walker have reached a consensus on some of the risk management issues:

Last week I gave Barbara the responses to our risk questions…

She has independently reached many of the same risk management concerns I have made and a few more. For example, that they are just pricing loans once and for all, not managing the heterogeneous portfolio risk effects, not bothering about correlation, not revealing true minimal loan standards or pricing and agrees that P2P is inherently much riskier than banking but they have far less experience and fewer safeguards.

So it’s a risk management mess.

22nd December 2016 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

Discussions about the what to put into the ExCo Risk Box continue into March 2017. A Senior Manager summed up the situation:

The problem at present appears to be that current viability, threshold, disclosure, client money and other tools only scratch the surface of such issues without getting rid of the underlying harm or detriment.

29th March 2017 – E-mail sent from Kim Heffernan – Senior Manager (Lending & Intermediaries department)

It is with some surprise that a Regulatory Risk Adviser removed the Risk Box from the briefing:

I have removed the risk box and annex…

31st March 2017 14.08 – E-mail sent from Lowri Jones – Regulatory Risk Adviser

An action which is promptly objected to:

I don’t know what the proper process for these things are and don’t want to get involved in that debate. However, by way of background – the risk box and annex was added with the express agreement of Supervision and Authorisations and following a discussion at the P2P Steering Group.

The intent was to ensure the discussion at Risk Co was appropriately informed and to highlight a particular problem – which is that no-one is picking up the broader issues. It was not controversial.

31st March 2017 14.19- E-mail sent from Natasha Pesaro – Manager (Risk & Compliance Oversight)

I’ve just been dragged into it this afternoon – let’s chat on Monday

31st March 2017 14.32 – E-mail sent from Lowri Jones – Regulatory Risk Adviser

Sure – it seems both embarrassing and disappointing

31st March 2017 14.19- E-mail sent from Natasha Pesaro – Manager (Risk & Compliance Oversight)

I get the sense that it’s an over-reaction (even Jose’s mail says it’s not not controversial) and we’ve made it worse by drawing attention to it

31st March 2017 15.21 – E-mail sent from Lowri Jones – Regulatory Risk Adviser

The meeting, held a few days later, did not go well. Words like ‘awkward’ and ‘uncomfortable’ are used. Walker Sigismund received a warning to calm his efforts.

This warning was given by Jose Morago, who describes himself as someone who had “led the FCA’s approach to Enterprise risk management, including the risk reporting to FCA Board and Executive Committee” during his tenure at the FCA. He now works at the international financial services provider Allianz.

Thanks Walker,

I attended the meeting today. The P2P discussion was positioned as an update (not for approval). I should say that it was a bit of an awkward and uncomfortable discussion. ██████████ There was a fair amount of discussion about [FCA rules on Client Money – CASS], approach/timing to forbearance and issues of unregulated [Collective Investment Schemes – CIS}. The discussion was cut short (as Jonathan had to leave) with no clear conclusion.

In terms of the risk box, again it was an awkward situation as not all the directors had a copy of your points (see below). Julia and Karina pressed the team on our points. Phil confirmed that they are taking on board/agree with all the points. Overall, I still am confused about the next steps and who really makes decisions on P2P.

Walker, your work and robust challenge on the P2P is really appreciated. However this is also a bit of political/sensitive topic internally, which requires careful stakeholder engagement from our side.

3rd April 2017 – E-mail sent from Jose Morago, Head of Enterprise Risk

A senior associate at the FCA, only a few months prior, had commented following a firms successfully lobbying efforts to remove Mr Sigismund from a different case:

I find it incredibly unfortunate that the FCA allowed themselves to be pushed around by a firm (with the complicit actions of the PRA [Prudential Regulation Authority]) as regards individuals assigned to support the supervision of that firm.

While there may have been diplomatic reasons for the decision to ask Walker not to be involved with the case going forward, I do not believe his conduct with this firm was ever not professional both in person and in his analysis – his only transgression seems to have been asking uncomfortable questions of them – something I think we are all here to do.

7th October 2016 – E-mail sent from [“LJ”] – Senior Associate (Retail & Authorisations)

Walker Sigismund, undeterred, continued to raise warnings:

Barbara,

In respect of your risk findings. Last week Fod and I both can (sic) to the conclusion that we needed to translate your and my risk findings into a policy context if we want them to land effectively, because at the moment very few people get their importance.

30th May 2017 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

A week later and P2P is still “a somewhat contentious issue“. This e-mail was sent straight to Andrew Bailey, the CEO.

Dear Andrew [Bailey],

I am sending you this e-mail which includes our analysis of peer-to-peer lending (risk box in 7.1-7.5 plus annexes). This will be discussed in the ExCo meeting next week.

Unfortunately I will not be there to explain it as I will be in the second module of my INSEAD course.

As you can imagine, this is a somewhat contentious issue. While we do not necessarily disagree with the first CP proposal of policy, we are still concerned that consumers stepping in the PtP world do not know that they are potentially exposed to high risks and we believe that they cannot be expected to understand the risks even with enhanced disclosure. The current regime may no longer be fit for the evolved business models, even with some patching.

Our analysis is based on a large number of sources including the real cases in Authorisations (one of my managers lead on this until February). We however acknowledge that Auths has made major strides in getting business models in a better place and we have followed these developments. Regrettably, this takes away some, but not all of our concerns.

…

I frankly would not mind being overruled by ExCo (because it would be on the basis of a fully informed view) but it is our remit to challenge proposals if we feel the risks are not fully mitigated.

7th June 2017 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight)

In response to this it seems Barbara is bypassed as a meeting is called without her. Did the Board doubt the judgment of high risk?

I just had a chat with Jonathan

This morning Andrew called Chris and Jonathan in for a meeting following my note about PtP.

He basically wanted to know if Jonathan liked the Policy proposal. Jonathan had not seen the full analysis we made but said he thought the risks were not mitigated in the Policy proposal even though CP1 was now better. Jonathan was quite taken aback by the assertion in the ExCO paper that no risks/harms have crystallised and said that is blatantly untrue. Andrew apparently is not keen on limiting retail investment. He however seemed to accept Jonathan’s views in the meeting which are a subset of our concerns.

Jonathan made a comment to me that the Board was ok with the CP1 proposal but I find that hard to believe (I don’t think they have even seen it).

I am uncomfortable that the meeting was set up without me, but I think this was because Andrew wanted to see if I was on my own expressing those concerns.

9th June 2017 – E-mail sent from Barbara Frohn – Director (Risk & Compliance Oversight)

Walker Sigismund replied to this, concerns aplenty:

Fod and I met with Jonathan Phelan ten days ago, who described his concerns at length, which in his own words included most of ours. He was also very concerned that in Supervision they had a very small set of tools to use and in any event could not carry on the intense interaction that was possible in Authorisation. He promised to write up these concerns and get them into the ExCo paper. We have not checked why that did not happen, but it does provide a potential avenue of discussion with Jonathan Davidson.

9th June 2017 – E-mail sent from Walker Sigismund – Manager (Risk & Compliance Oversight)

The Head of Retail Lending Supervision chips in with his view – the FCA’s approach isn’t working and needs resetting:

Fod raised the global issues around P2P last week in the Steering Group meeting. I think Fod and I share the view that chipping away, firm by firm, is inefficient, resource-intensive, and wont improve the industry. We feel that the priority need is for FCA to press ‘re-set’ on the P2P landscape – our regulatory expectations, firms’ obligations, and consumers’ rights.

CP {consultation paper] 1 and CP2 will allow us to do this. And so we are in a good place in theory. However, we have two concerns. The first is timing. This process will take a long time and in the meantime we have the slow chipping away on a firm by firm basis. The second and perhaps more important point is achieving a consensus on what our regulatory expectations should be. We have divergent views at all levels, right up to ExCo.