Auditing firm Moore Stephens LLP has robustly defended a £15m High Court claim which alleged they acted “negligently” and with a lack of “professional scepticism” when they signed off the accounts of the now failed peer-to-peer lending firm Lendy.

This site is financed by donations to the ‘Cheese Fund‘ or you can buy me a coffee here

Reporting by Daniel Cloake

We previously reported on the claimants case in ‘Lendy auditor caused £15m loss to investors, court papers claim‘.

We also reported that the defendant had been given an extension of time to file their defence in ‘Lendy auditor given new deadline in £15m negligence case‘.

The defence has now been filed. We’re publishing both pleadings in the interests of open justice:

In a 29-page-document prepared by barristers Rebecca Sabben-Clare KC and Pippa Manby on behalf of the firm Moore Stephens, now known as MSR Partners LLP since their merger with BDO LLP, we’re told in essence that whilst the auditing firm did make mistakes, it was the dishonest conduct of the former directors who are to blame for any losses.

“The conduct of Lendy was driven by its directors and their conduct was the sole cause of Lendy’s actions as a matter of fact and law...Every allegation made by the Claimant that the financial statements were defective lies primarily against the Directors”

It’s worth noting that the directors are not parties to this claim and do not have an opportunity to defend themselves. They have previously denied any accusations of wrong doing. None of these claims have yet to be tested in court.

The claimant Manolete Partners Plc, who were assigned the claim by the joint administrators of Lendy, how have until December 6th 2024 to file a reply.

Criticism of the claimants case is raised in just the second paragraph which states that “much of the Claimant’s case is vague and embarrassing for want of particularity and is impossible for the Defendant properly to understand or to plead to“.

It’s further said that “the Claimant has wholly failed to plead a properly particularised and intelligible case that the Defendants’ breaches caused Lendy to suffer loss.“

Several reasons are given including that:

(a) the claim is largely for losses suffered by investors, rather than Lendy;

(b) losses suffered by Lendy’s investors were not caused by the Defendant’s conduct as a matter of fact or law;

(c) any such losses are in any event outside the scope of the Defendant’s duty and/or too remote to be recoverable; and

(d) such losses should have been mitigated by action against the borrowers and the Directors.

Model 2 errors

The defendant candidly “admits to breaches of duty on its part in relation to its audit work

concerning the treatment of Model 2 loans“.

Model 2 relates to a structure where investors’ money is lent directly to the borrower with the platform just acting as an agent.

Moore Stephens had incorrectly included these model 2 loans in the financial statements as if they were loans in which Lendy acted as principal.

It’s agreed that the inclusion of these loans in the financial accounts “did not give a true and fair view of Lendy’s financial position“.

It’s admitted that the difference between the model 1 and model 2 loans “ought to have been identified and its consequences explained” in the accounts.

It is however denied that this mistake caused any losses as “the directors of Lendy and other senior employees were aware of Lendy’s true position in all regards“. The defence also claims that the FCA were aware of the true position too.

The Audits

Discussing the alleged problems with the 2016 audit we’re told that “the Defendant

relied upon information provided to it by Lendy” which apparently did not include a pertinent communication from the FCA to Lendy dated 13th February 2018.

This communication is said to have contained a bombshell revelation that the FCA were “minded-to-refuse” full authorisation of the peer-to-peer lending platform.

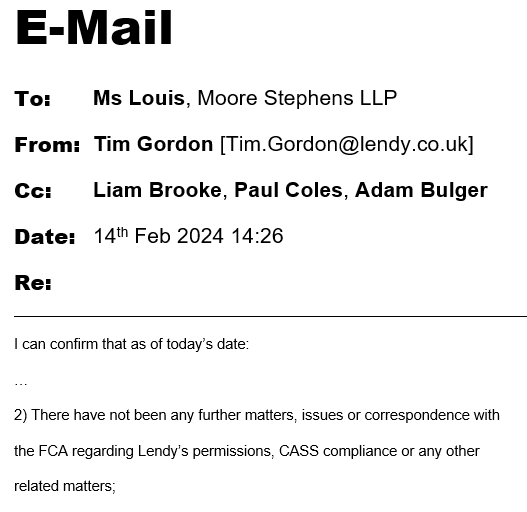

Four-days-earlier “Lendy’s management (including the Directors and its Head of Compliance Paul Coles)” had apparently told the auditor that “the FCA was likely to grant full authorisation in Q2 2018“.

Blame is laid directly at the door of Tim Gordon, 45, who it’s said had made “a dishonest misrepresentation” by “dishonestly informing the Defendant on 14 February 2018, before the FY2016 Audit Report was signed, that there was no development as regards Lendy’s FCA permissions.“

It is said Mr Gordon sent the following e-mail containing “a dishonest and deliberate misrepresentation of the state of Lendy’s discussions with the FCA“.

The auditors say in no uncertain terms that “this [e-mail] was untrue, and known to [Gordon] to be untrue, because Lendy had received notification from the FCA that it was initiating the process of preparing the [minded-to-refuse] Letter“.

This information was described as being “deliberately and intentionally concealed” from the auditors.

The FCA never issued a minded-to-refuse letter instead granting the platform full authorisation, something the FCA’s then chief exec Andrew Bailey said was done to prevent consumer harm. The FCA finally pulled the plug on the platform in May 2019.

In the defence it’s further claimed that the Head of Compliance Paul Coles, 54, and fellow director Liam Brooke, 42, had “dishonestly … failed to correct Mr Gordon’s false statement” despite being CC-ed into the e-mail.

The auditors do candidly say that letter aside they were aware of prior problems identified by the FCA at the firm and had “failed to obtain sufficient appropriate audit evidence and failed to exercise adequate professional scepticism” by failing to consider whether these had been addressed by Lendy.

Marshall Island Payments

Whether the directors had misappropriated £6.5m of company money via off-shore entities registered in the Marshall Islands was the subject of a separate high court case in 2020, and the subject of extensive reporting by this site – see The Marshall Island Mystery.

The claim alleged that the auditors should have identified these Marshall Island payments as improper and reported them to the FCA.

In response the auditors say that if the payments were “fraudulent or improper” then “the Directors would have concealed their true nature from the Defendant by whatever means were necessary.” and in any event would have reported their concerns to Mr Coles “in the first instance“.

It is denied that had such a report been ultimately made to the city regulator then this would have caused the FCA to “immediately” suspend Lendy’s business and prevent it from offering further loans.

Lendy losses or investor losses?

The auditors assert that the alleged losses were suffered by the investors, not Lendy. The claim had specified that at the date of entry to administration the purported loss was estimated at £15,599,571.

It’s said “the Claimant has not identified any basis on which it is entitled to claim compensation for losses suffered by the Investors.“

“Any losses suffered by the Investors are the consequence of the quality of the lending and/or the acts of the Borrowers” and not the auditors, we’re told.

Mitigation

The auditors say the claimant “is put to strict proof” that Lendy (and its officeholders) have taken reasonable steps to mitigate the alleged losses.

It’s said this proof should include what steps have been taken to pursue the borrowers for unpaid loans, including enforcement steps against relevant security and any relevant third party claims; its pursuit and enforcement of the claim against the directors; and whether they sought to reduce any penalties and interest imposed by HMRC.

Counterclaim

Not content to just defend the claim the auditors have also issued a counterclaim.

The counterclaim states that because Lendy affirmed that various documents provided by the platform were true, in the event that the auditor is found liable then they are “entitled to damages to the same extent”.

Some would say the entire point of having an audit is to prevent directors from being able to make unsubstantiated claims about their business.

So what happens next?

The claimants have until 6th December 2024 to “file and serve its Reply“ to the defence statement.

We’ll aim to obtain copies of this document shortly after it has been filed at court. You can support us with the cost of this endeavour by buying us a coffee or donating to the cheese fund.

Assuming the case proceeds the next step after exchange of pleadings will be for a so-called costs and case management hearing likely to be held in the first half of 2025.

Were this case to proceed to a trial then it might be 2026 or later before we can take our seats in the public gallery. We’ll aim to keep you updated.

Case details

Manolete Partners Plc v MSR Partners LLP

Case Number: BL-2024-000191

MSR Partners LLP are represented by Clyde & Co

Manolete Partners Plc are represented by Gateley