Top tax barrister Robert Venables KC, 78, of Old Square Tax Chambers is currently facing three counts of dishonestly cheating the public revenue in criminal proceedings before a jury at Southwark Crown Court.

Our reporting of this case:

✍️ Jan 2025: Barrister accused of falsifying tax returns – the indictment revealed

✍️ May 2026: Trial date set for barrister accused of falsifying tax returns

✍️ May 2026: Barrister’s barrister tells jury: “There is nothing legally wrong with avoiding tax and exploiting loopholes”

✍️ May 2026: Wise gardener gives evidence in KC Tax Cheat case

✍️ June 2026: Venables’ Bookkeeper Gives Evidence in KC Tax Cheat Case

✍️ June 2026: R v Venables KC: The HMRC Interviews: “wouldn’t it be wonderful if tax law were always simple and logical”

✍️ June 2026: HMRC’s criminal probe against Tax KC had “Red Risks”, jury told

✍️ June 2026: HMRC’s ‘menacing’ correspondence meets Tax KC’s threats of defamation, jury hears

✍️ June 2026: R v Venables KC: The Agreed Facts

✍️ June 2026: Top Tax KC: “I’ve been cancelled” as jury told of humble beginnings

✍️ June 2026: Tax KC’s ‘private working notes’ were attempt to ‘pull the wool over the eyes of HMRC’, jury told

✍️ July 2026: Jury to consider verdicts as the trial of KC accused of dodging £2m in tax comes to an end

✍️ July 2026: “It has become clear that a serious problem has arisen between you” – Judge urges jury to be respectful

✍️ July 2026: “Now you’re a jury of 11” – KC Tax Trial latest

✍️ July 2026: Venables jury down to 10

✍️ July 2026: Venables Trial Collapses

Please buy us a coffee to support crowd-funded journalism

Reporting by freelance journalist Daniel Cloake

Robert Venables (left) with barrister Stuart Biggs KC outside Southwark Crown Court

Dean Steven Wise, a former gardener and labourer to Robert Venables KC, gave evidence to Southwark Crown Court on Thursday. Appearing in a brown and cream checked shirt Mr Wise was in the witness box for 91 minutes.

Mr Wise said that during his interview for the job in 2011 he was told he would be paid a rate of £10.78/hr from a trust but that “I didn’t understand anything about trusts or what trusts were…I was very sceptical. I said I would have to call them back later”.

We were told Mr Wise spoke to his father’s accountant and “he basically he said it was a legit thing that some people use”.

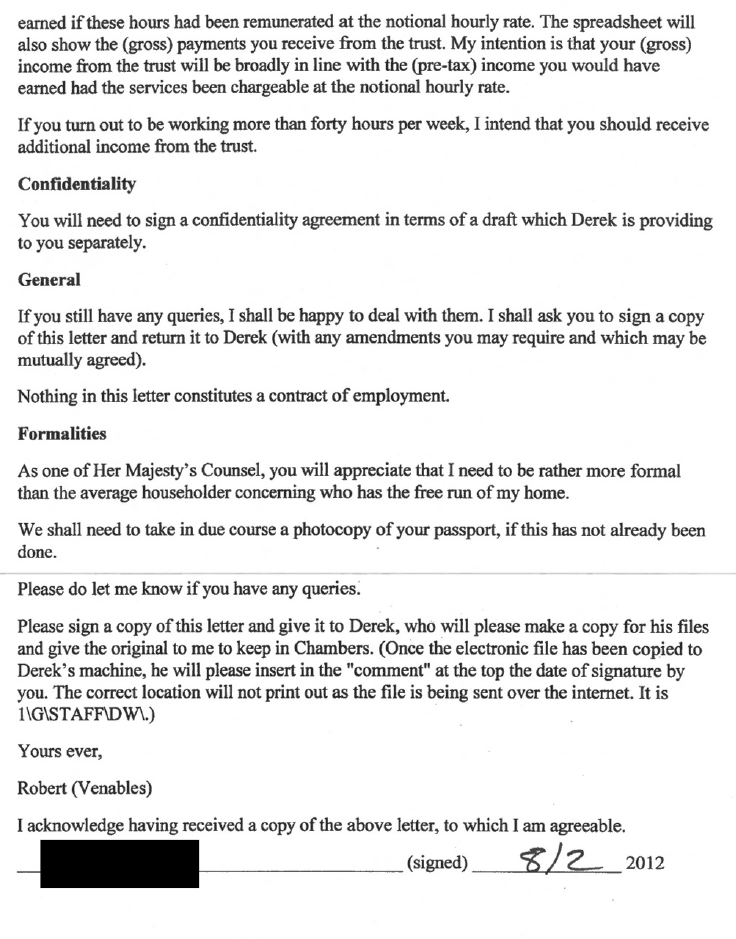

On 7th February 2012, almost a year into the job, Mr Wise says he was given a letter to sign from Venables. Wise said he felt under pressure to agree there and then: “I was put on the spot, I felt if I didn’t sign the letter, I wouldn’t be able to carry on working here.”

The letter declared that he would be rendering services as neither an employee, or as a self-employed contractor, and would receive “no remuneration as such”. It was said in the letter it was the intention that he would be given a right to income from the so-called St Bartholomew’s Trust.

One benefit was that Mr Wise would pay no National Insurance, unlike income from employment. Although Wise was told if he worked more than 40 hours per week he would receive additional money from the trust.

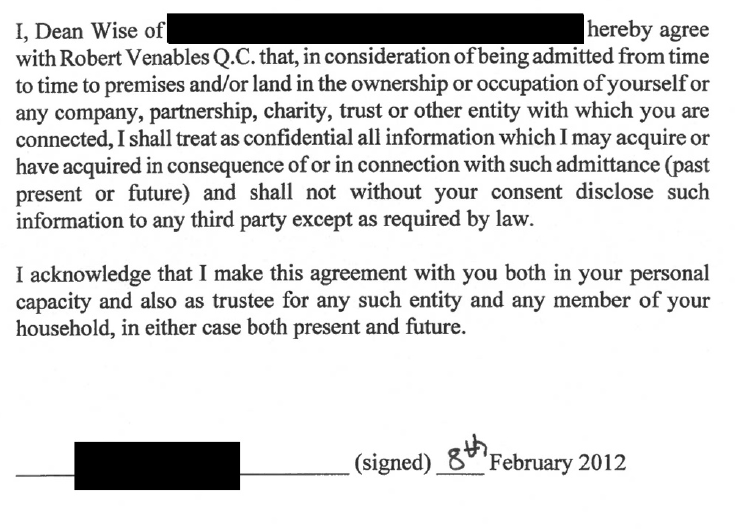

The third page of the letter contained a confidentially agreement.

It was confirmed that the trust would deduct 20% tax prior to giving Mr Wise the money, and that he would therefore receive a tax refund at the end of the year if he had no other income. It was said Mr Venables wrote he would offer to “assist you with your tax return”.

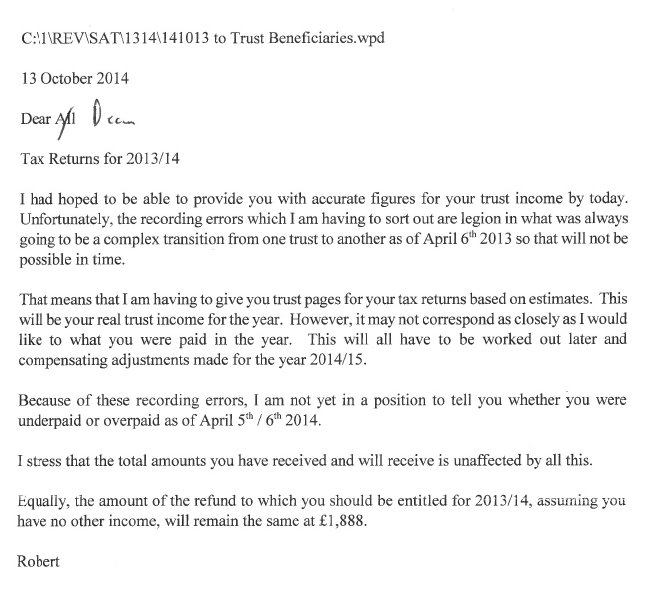

On one occasion, for the 2013/2014 tax year, Venables sent a letter to Mr Wise which blamed “reporting errors” for a delay in providing “accurate figures“.

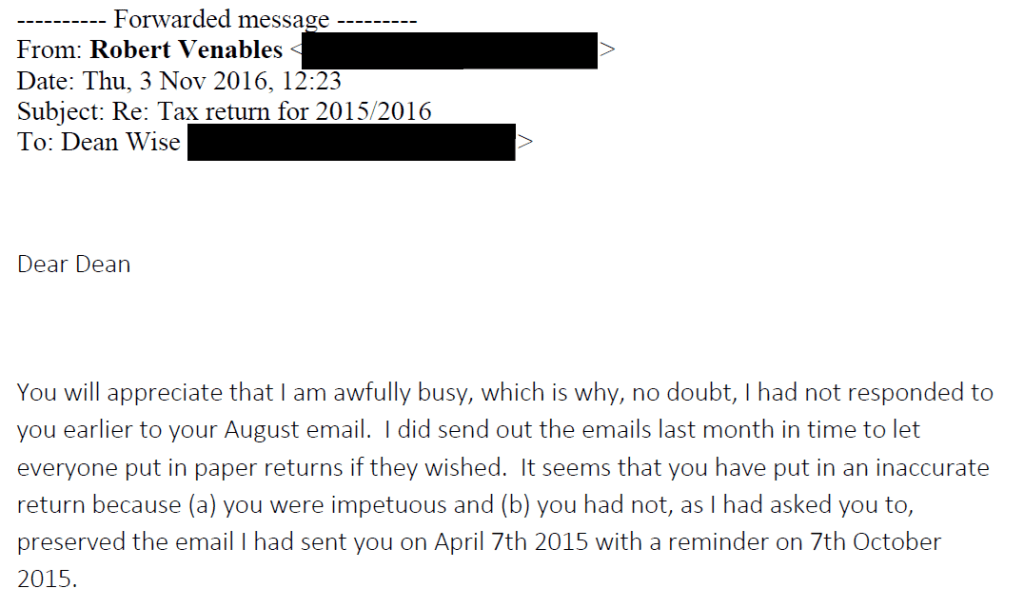

Delays were apparent the following year too. The jury were shown an email from Venables regarding the 2014/2015 tax year:

One tax return submitted by Wise, was rejected by HMRC on the basis that a supplementary trust page was needed. Wise was warned he would start to receive a £100/day penalty should the problem not be rectified.

We heard Venables dictated a letter for Wise to type in response. He wrote the challenge was an “entirely futile procedure” and that if HMRC “was not happy please explain on the trust pages where I should have entered the income in question”.

Wise’s somewhat wise premonition that he had a “bad feeling there’s going to be a real headache for me to sort out later on” came true when submitting a tax return, without guidance from the tax KC, after he had left his role with Venables.

Replying to an emailed request for help Venables told Wise: “It seems you have put in an inaccurate return” before adding as “you were impetuous”. The email ended with an unevidenced attack on the character of Wise.

Under cross-examination from barrister Stuart Biggs KC, representing Venables, it was conceded that the trust arrangements were odd – “It’s weird isn’t it, what they’re explaining to you [during the interview]?”

Wise agreed, adding that despite the role he moved on to attracting a lower salary he was able to pay NI, and obtain a pension.

The court also heard evidence from Mr Christopher Lewis Jones, a long-standing friend of Mr Venables “for almost 50 years“.

Jones was asked by Mr Christopher KC, representing the Crown, how he came to sign a 42-page document entitled ‘The Christopher Lewis Jones 2019 Deed Poll’.

Jones said that “Robert contacted me some time prior to this date [of signing] and asked me for a small favour. He’s an old friend and I trusted him, and trust him completely“. He described the document as “some financial matter that would help him” confirming he agreed to help sign the documents.

Asked if he had read the document he said “not every single word, but I would have scanned through it“.

We were told that “in the initial conversation Robert explained that part of the favour was ten £5 notes in envelopes” which were left with Robert, and confirmation of this was detailed in the deed poll.

An AI impression of how this might have looked

In cross-examination by Mr Biggs KC, Mr Jones was asked about how he had described Venables in his first witness statement: “As an old friend who I always found to be unscrupulously honest” adding orally he was “extremely hard working. No one worked as hard as him… He has been extremely successful but my god he’s worked for it“.

The circumstances of how this praise appeared, or had not appeared, in the witness statement was criticised by Mr Jones.

We were told two HMRC officers had attended his house to take a statement. Jones said he told them Venables was “Absolutely meticulous about dots on the i’s and crosses on the t’s“. One of the HMRC officers apparently replied “there’s no need to record that“, and so it was left out of the statement.

“That doesn’t sit well with me so I added it to a later draft of the witness statement and it’s still there today,” said Jones.

During the questioning Jones said he “had to ask them to sit down. I had to ask for time to read things. I was under pressure to answer in the way they wanted.”

During this exchange a member of the jury passed up a note explaining it made them “uncomfortable” that the witness statements were not being provided to the jury and only extracts were being read out. Mr Justice Calver explained “the evidence you have to rely on is the evidence you hear from the courtroom…I’ll be alive to any confusion that might arise. That is the procedure we adopt in the criminal courts.“

The defendant Robert Venables KC, wearing a black suit, sat at the back of the court in an area normally reserved for lawyers, typing notes on a laptop.

The trial continues.

The CPS are represented by Julian Christopher KC, Marika Lemos KC, and Michael Hick. Mr Venables is represented by Stuart Biggs KC and Erin McKee.

The mouseinthecourt attended Southwark Crown Court on Thursday 28th May 2026.

The work on this site is protected by copyright laws and treaties around the world. All such rights are reserved.

You may print off one copy, and may download extracts, of any page(s) from our site for your personal use and you may draw the attention of others within your organisation to content posted on our site.

You must not modify the paper or digital copies of any materials you have printed off or downloaded in any way, and you must not use any illustrations, photographs, video or audio sequences or any graphics separately from any accompanying text.

Our status (and that of any identified contributors) as the authors of content on our site must always be acknowledged.

You must not use any part of the content on our site for commercial purposes without obtaining a licence to do so from us or our licensors.