Top tax barrister Robert Venables KC, 78, of Old Square Tax Chambers is currently facing three counts of dishonestly cheating the public revenue in criminal proceedings before a jury at Southwark Crown Court.

Our reporting of this case:

✍️ Jan 2025: Barrister accused of falsifying tax returns – the indictment revealed

✍️ May 2026: Trial date set for barrister accused of falsifying tax returns

✍️ May 2026: Barrister’s barrister tells jury: “There is nothing legally wrong with avoiding tax and exploiting loopholes”

✍️ May 2026: Wise gardener gives evidence in KC Tax Cheat case

✍️ June 2026: Venables’ Bookkeeper Gives Evidence in KC Tax Cheat Case

✍️ June 2026: R v Venables KC: The HMRC Interviews: “wouldn’t it be wonderful if tax law were always simple and logical”

✍️ June 2026: HMRC’s criminal probe against Tax KC had “Red Risks”, jury told

✍️ June 2026: HMRC’s ‘menacing’ correspondence meets Tax KC’s threats of defamation, jury hears

✍️ June 2026: R v Venables KC: The Agreed Facts

✍️ June 2026: Top Tax KC: “I’ve been cancelled” as jury told of humble beginnings

✍️ June 2026: Tax KC’s ‘private working notes’ were attempt to ‘pull the wool over the eyes of HMRC’, jury told

✍️ July 2026: Jury to consider verdicts as the trial of KC accused of dodging £2m in tax comes to an end

✍️ July 2026: “It has become clear that a serious problem has arisen between you” – Judge urges jury to be respectful

✍️ July 2026: “Now you’re a jury of 11” – KC Tax Trial latest

✍️ July 2026: Venables jury down to 10

✍️ July 2026: Venables Trial Collapses

Please buy us a coffee to support crowd-funded journalism

Reporting by freelance journalist Daniel Cloake

Robert Venables (left) with barrister Stuart Biggs KC outside Southwark Crown Court

Three documents, said to have been written at the time of the formation of a scheme designed to save a top tax barrister millions of pounds in tax, have been the subject of intense scrutiny before a jury at Southwark Crown Court.

Facing three counts of cheating the Public Revenue, Robert Venables KC has spent his seventh day in the witness box giving evidence.

Venables was asked about comments he himself made in three documents written back in June 2014. Annotations had been made within yellow highlighted text.

“Some people think aloud … I make notes, I type away” he said of the documents adding “This is, as it were, my private working notes…This is not an extended opinion written for the benefit of a third party.”

One section of the document, located in a discussion about partnerships, explained:

A receives or is entitled to receive at any time any benefit provided or to be provided (directly or indirectly) out of B’s profit share or the part;

Asked about whether the source of £500k from Breamgale Limited, a company run by Robert’s brother, was from “B’s profit share” the defendant said to Mr Christopher KC, appearing on behalf of the Crown:

“You have to distinguish between law and equity. You would have had to study this when qualifying as a barrister”.

Venables was also asked to explain what is meant by the term ‘power to enjoy’ … He said: “I have given extensive reasons why I wouldn’t have power to enjoy” adding “why would you think I do?”

“Because you want to be able to use the money Mr Venables” replied Mr Christopher KC.

Venables, recognising the complexity of some of his answers, said “I’m sorry members of the jury this is really, really technical. You must be completely bemused by all this… If I had known this was going to be considered by a jury in due course I wouldn’t have used all these long words.”

Settlor v Settlement

This case is not concerned with whether the schemes worked or not – the jury have been told that, as a point of law confirmed by the Court of Appeal, they did not work. The crux of this case is whether Venables knew at the time that they did not work.

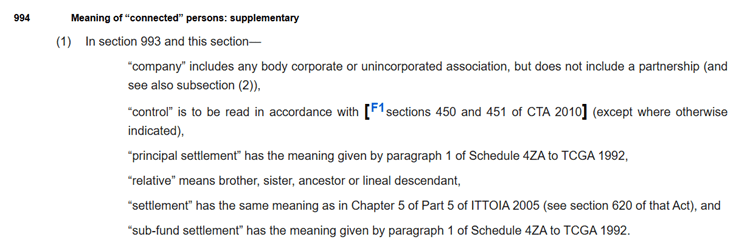

One of the details looked at was section 994 of the Income Tax Act 2007. It can be seen that the term settlement is defined, but not the term settlor.

“s994 is quite clear” said Venables, “Settlement has the same meaning as s620… It doesn’t say settlor has the same meaning. Parliament has adopted the same meaning as settlement but not the same meaning of settlor”.

Christopher KC: “And that’s what you thought back in 2014?”

“Yes”

Paragraph 17 from Venables’ defence statement, was also shown to the jury, who were told that D stands for the defendant:

D accepted that the Settlement Provisions applied to the deemed amount of profits of a trust for the years in which D was entitled to an interest in possession under it. However, the amount of taxable trust income which was deemed to be his by virtue of the settlement provisions was identical to the amount of his deemed taxable income from the trust the settlement provisions apart. This means that the settlement provisions had no practical effect in relation to such income

The first line of this paragraph caught the eye of Mr Christopher.

“‘D accepted’: that’s past tense. It was plainly your belief at the time of filling in your tax returns…not D accepts, it says accepted.”

Venables: “Let us see where this is going…”

Christopher: “If it’s wrong you should tell us.”

It was put to the defendant that “you must surely have looked very carefully at every sentence in your defence statement”, which it was explained, had been drafted by his solicitors.

“If I had the time” replied Venables, citing that he had only been asked to provide the statement some 40 days ago.

In a somewhat tetchy exchange a comparison was made between the documents produced in 2014, and what was said in his defence statement: “The two are inconsistent aren’t they?”

It was eventually conceded by Venables that “as it stands, on its literal interpretation, they are inconsistent.“

It was put to Venables that the documents were produced as part of “an exercise carried out in 2014 to work out how you might pull the wool over the eyes of HMRC”.

It was also put by Mr Christopher “I suggest your tax returns were dishonest.”

“They were not” replied Venables, denying this was part of a scheme of “misdirection in the event of enquiries”.

In re-examination by Mr Biggs KC, representing the defendant, Venables was asked if he had “come to the conclusion”, in these 2014 documents, that “there were problems with your scheme and they didn’t work anymore?”

“No, I thought it did work but could be made better.”

Venables was asked “when you express a conclusion in these [2014] notes… was that your view at the time?” “Yes, why should I misrepresent this to myself?”

At one point Venables referred to Section 1264 of the Corporation Tax Act 2009. How could he remember 1264 off the top of his head – we were told Merton College, Oxford was founded in 1264 … “that’s my little aide-mémoire”.

Biggs said the prosecution had suggested that Venables had been “coy or incomplete” about disclosing the role of Citadel Limited in his interviews with HMRC. “You told the jury the point of Citadal was not tax avoidance but to protect you against the enablers legislation…When you devised Citadal for this purpose did you tell HMRC about it?”

“No, no reason I should…This is their legislation, they are happy with it. If it doesn’t work as well as they were expecting that’s up to them.”

The HMRC Enablers Legislation is a set of anti-tax-avoidance rules designed to penalise not just the taxpayer using an abusive tax scheme, but also the people that helped to create it. By having Citadal Limited provide the advice, rather than Robert Venables personally, this meant the company would face any penalties, and not him.

One supposed benefit of this arrangement was that corporation tax would apply, at 20%, rather than the higher rate of income tax, set at 45%. The assumption that this benefit was legitimate has now been found to be wrong due to the application of something called the Settlements Code.

Biggs asked “If you knew the settlements code did apply would you have done this.”

“Good heavens no” came the reply.

Concluding his re-examination, and the evidence of the defendant, Biggs asked “in relation to any of these three counts” did you make any of these arrangements, or put these things in place “thinking as a matter of law this doesn’t work but I’m going to carry on anyway?”

“Absolutely not, and everybody who knows me knows this is not the way I work” said Venables.

During the mid-morning break, the jury passed a note to the judge expressing concern about the “excessive heat” when travelling in, especially if the “heat does reach 38 degrees as predicted”.

Prompting laughter in the courtroom Mr Justice Calver told the jury “I do understand your concerns…you ought to try wearing this outfit in the heat”, referring to his full set of red High Court robes.

The trial continues.

The CPS are represented by Julian Christopher KC, Marika Lemos KC, and Michael Hick. Mr Venables is represented by Stuart Biggs KC and Erin McKee.

The mouseinthecourt attended Southwark Crown Court on Monday 22nd June 2026.

The work on this site is protected by copyright laws and treaties around the world. All such rights are reserved.

You may print off one copy, and may download extracts, of any page(s) from our site for your personal use and you may draw the attention of others within your organisation to content posted on our site.

You must not modify the paper or digital copies of any materials you have printed off or downloaded in any way, and you must not use any illustrations, photographs, video or audio sequences or any graphics separately from any accompanying text.

Our status (and that of any identified contributors) as the authors of content on our site must always be acknowledged.

You must not use any part of the content on our site for commercial purposes without obtaining a licence to do so from us or our licensors.