Top tax barrister Robert Venables KC, 78, of Old Square Tax Chambers is currently facing three counts of dishonestly cheating the public revenue in criminal proceedings before a jury at Southwark Crown Court.

Our reporting of this case:

✍️ Jan 2025: Barrister accused of falsifying tax returns – the indictment revealed

✍️ May 2026: Trial date set for barrister accused of falsifying tax returns

✍️ May 2026: Barrister’s barrister tells jury: “There is nothing legally wrong with avoiding tax and exploiting loopholes”

✍️ May 2026: Wise gardener gives evidence in KC Tax Cheat case

✍️ June 2026: Venables’ Bookkeeper Gives Evidence in KC Tax Cheat Case

✍️ June 2026: R v Venables KC: The HMRC Interviews: “wouldn’t it be wonderful if tax law were always simple and logical”

✍️ June 2026: HMRC’s criminal probe against Tax KC had “Red Risks”, jury told

✍️ June 2026: HMRC’s ‘menacing’ correspondence meets Tax KC’s threats of defamation, jury hears

✍️ June 2026: R v Venables KC: The Agreed Facts

✍️ June 2026: Top Tax KC: “I’ve been cancelled” as jury told of humble beginnings

✍️ June 2026: Tax KC’s ‘private working notes’ were attempt to ‘pull the wool over the eyes of HMRC’, jury told

✍️ July 2026: Jury to consider verdicts as the trial of KC accused of dodging £2m in tax comes to an end

✍️ July 2026: “It has become clear that a serious problem has arisen between you” – Judge urges jury to be respectful

✍️ July 2026: “Now you’re a jury of 11” – KC Tax Trial latest

✍️ July 2026: Venables jury down to 10

✍️ July 2026: Venables Trial Collapses

Please buy us a coffee to support crowd-funded journalism

Reporting by freelance journalist Daniel Cloake

Robert Venables (left) with barrister Stuart Biggs KC outside Southwark Crown Court

Jurors at Southwark Crown Court have been read significant amounts of correspondence between Robert Venables KC and HMRC. Having only just been sent copies the mouseinthecourt has made an editorial decision to publish all 121 pages of it, subject to minor redactions.

Download all 121 pages (20mb file)

With complaints about “menacing” letters, allegations of “bullying tactics”, and references to potential defamation claims. We’ve published the documents and highlighted key passages from the trial below:

Pages 1 – 4 : 8th April 2011

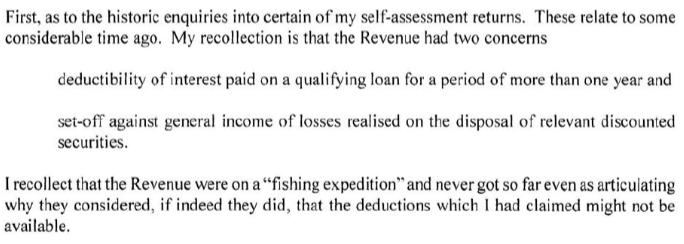

RV complains that a previous request for documents was in fact a “fishing expedition“:

And a complaint was made that the purpose of the enquiries was “simply to harass taxpayers…“:

Venables said he would “like to consider myself a person or more than average fortitude in dealing with over-zealous civil servants” having “asked myself what the effect of such a letter would have been on a less robust person. I shudder to think“

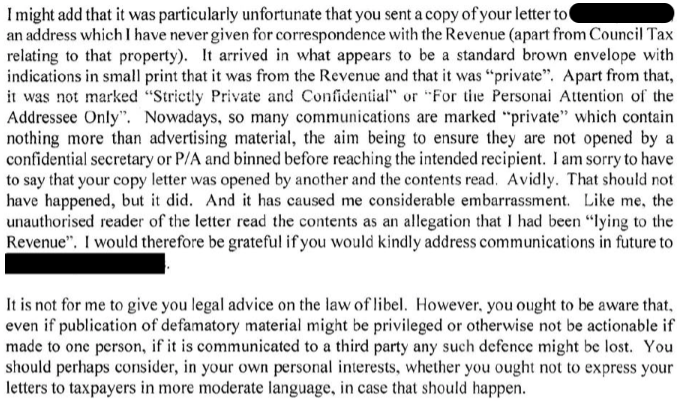

Complaint was made over the labelling of correspondence as ‘private’, having asserted that a member of his staff had read a letter from the revenue “avidly“. A veiled threat of a defamation suit was made:

The nub of the defence is also alluded to:

Pages 8 – 9 : 4th June 2018

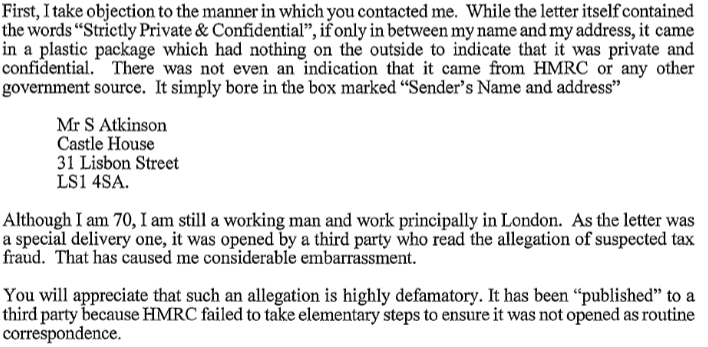

Further complaint is made of the labelling of envelopes:

The recipient at HMRC is “respectfully” reminded that a breach of confidentiality is a criminal offence.

The tone of the previous letter, sent by HMRC, is criticised as “menacing” and “clearly designed to intimidate“:

Page 18 : 7th October 2018

Venables says the tone of a previous letter, sent by HMRC, is “unnecessarily confrontational” and that HMRC’s assertion that “non-compliance with the notice may render me liable to penalties… does seem heavy handed“.

Page 26 : 7th November 2018

HMRC reply referring to the complaint about the tone of the letter, asking Venables to “accept my apologies for any mis-understanding in this regard“.

Pages 36 – 39 : 12th March 2019

Venables explains to the HMRC investigator that “the difficulty is not so much in explaining the position as in explaining it succinctly and to someone such as yourself who, so far as I know, has no legal qualification“.

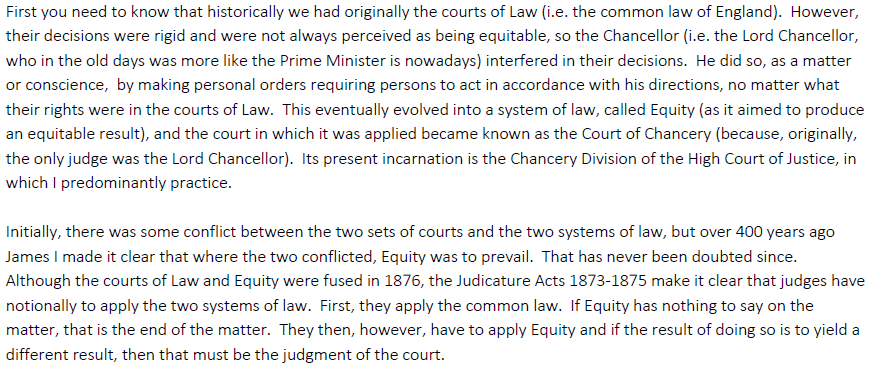

A lengthy explanation is given on the next page on the history of trusts, and how the Chancery Division of the High Court was formed. We’re told income tax was introduced “during the Napoleonic wars“

An anecdote was given about how “The presiding judge [of a constitution of the Court of Appeal] went out of his way to be rude to me and said that my submissions were as outdated as Gilbert and Sullivan” before the House of Lords “unanimously reversed” the decision and “went out of their way to say how much they had appreciated and relied on my historic analysis“.

Page 64 : 7th July 2021

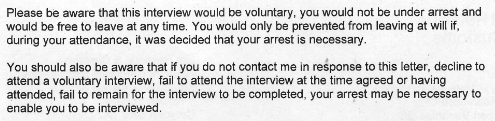

In a letter dated 7th July 2021 Mr Venables is formally accused of having “committed the offences of fraudulent evasion of income tax…” and is invited to a so-called voluntary interview.

Voluntary in so far as he is warned that he might be arrested were he fail to attend:

Pages 66 – 77 : 11th July 2021

Four-days later Venables replies saying he found the letter “most surprising, not to say “shocking”“. We’re told he “utterly repudiate the allegations which have been made“.

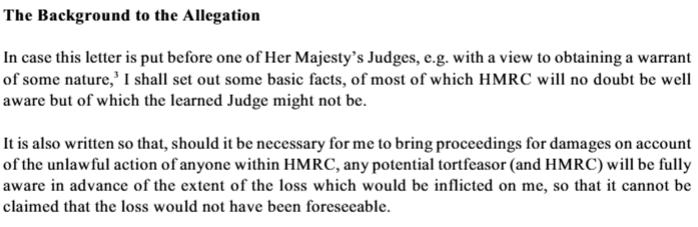

Venables sets out some “basic facts” in case “this letter is put before one of Her Majesty’s Judges” and also “should it be necessary for me to bring proceedings for damages on account of the unlawful action of anyone within HMRC“

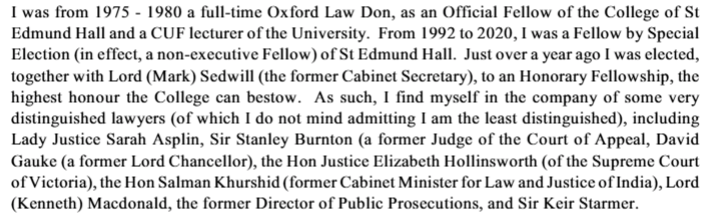

Venables goes on to explain how he considered himself to be in the company of “some Very distinguished lawyers” including Sir Keir Starmer (who had become leader of the opposition the year before).

Venables says he will refuse to attend the interview, and would only consider attending when provided with the “full particulars of the precise criminal conduct in which someone believes I have been engaged and make out that there is a real case for me to answer, in order to justify my wasting considerable time and incurring the considerable expense of engaging the services of a solicitor to represent me and attend the interview“.

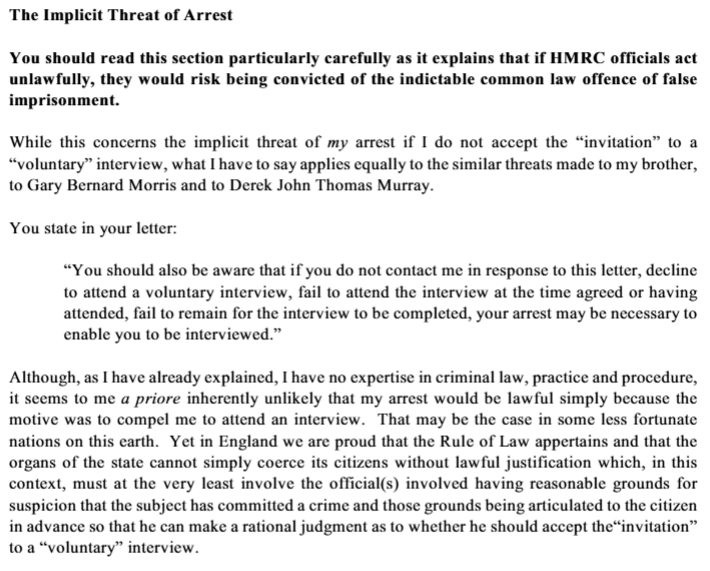

With regards to the “implicit threat of arrest” he says HMRC officials might face prosecution for false imprisonment were he to be detained. Reference is made to “less fortunate nations on this earth” where this could be considered lawful.

Damages wouldn’t only be compensatory, but might also be “exemplary“, the letter states:

Whether the letter attracted qualified privilege, a defence in defamation claims, is a matter for another day, we’re told:

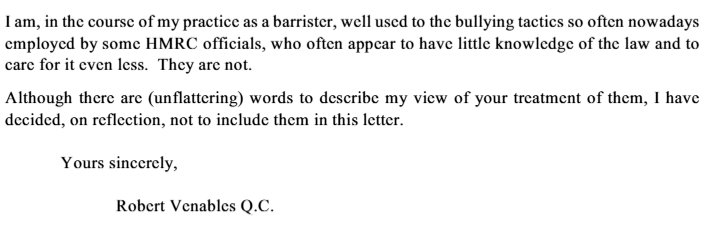

Venables accuses HMRC of “bullying tactics” but declines to provide his “unflattering” words:

Despite the misgivings Mr Venables did attend an interview on 24th July 2021. We hope to publish the transcript of the interview in due course.

Page 106 : 21st June 2022

In a letter from HMRC dated 21st June 2022 Venables is invited for second interview. Again, we hope to publish the transcript of the interview in due course.

Pages 108 – 121 : 8th July 2022

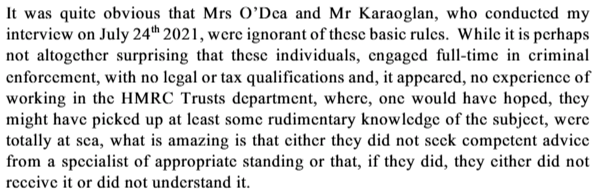

Following the second interview, a ‘Memorandum’ is sent to HMRC. In it Venables is critical of those who interviewed him:

The trial continues.

The CPS are represented by Julian Christopher KC, Marika Lemos KC, and Michael Hick. Mr Venables is represented by Stuart Biggs KC and Erin McKee.

The work on this site is protected by copyright laws and treaties around the world. All such rights are reserved.

You may print off one copy, and may download extracts, of any page(s) from our site for your personal use and you may draw the attention of others within your organisation to content posted on our site.

You must not modify the paper or digital copies of any materials you have printed off or downloaded in any way, and you must not use any illustrations, photographs, video or audio sequences or any graphics separately from any accompanying text.

Our status (and that of any identified contributors) as the authors of content on our site must always be acknowledged.

You must not use any part of the content on our site for commercial purposes without obtaining a licence to do so from us or our licensors.